FINANCE

Financial Tips for New College Students

What you'll learn: The student-friendly way to budget and save your way to financial freedom.

EXPECTED READ TIME: 13 MINUTES

Your class schedule is set, you’ve posed for your student ID, and you’ve pinned every coffee shop within a mile of campus (or your remote learning outpost). It’s an exciting time!

From newfound independence and diverse connections to career-transforming lessons, the college experience is unlike any other. But it’s also costly. The tuition, textbooks, tech, late-night study snacks, and early-morning coffees add up fast!

Whether you’re the first in your family to pursue a college degree, an international student finding your footing, or an adult learner returning to the books, this guide is for you!

From meal plans to financial aid, we’ll show you how to get a handle on your finances while in school so you don’t stumble into a mountain of bad debt.

The Importance of Financial Management as a College Student

You may have received a chores-based allowance throughout middle school or had a part-time gig in senior high. These experiences taught you the value of money and allowed you to fund small pleasures, but it was all under the watchful eye of mom and dad.

In college, the guardrails are gone. It’s just you and your money.

To truly take charge of your finances in this pivotal life chapter, you need to have an idea of what you’re up against.

Did you know the average annual cost of college, including books, supplies, and living expenses, is $38,270 per student? That’s a serious chunk of change — enough to run anyone into financial trouble without proper money management.

This is why budgeting, thoughtful planning, and building healthy credit habits are so important. Together, these tools set you on the path to lasting financial wellness.

Financial Challenges in College

Let’s talk financial hurdles in college. They can come at you fast.

Knowing what to watch out for can help you plan smarter. Here are six common financial challenges with ways to get around them:

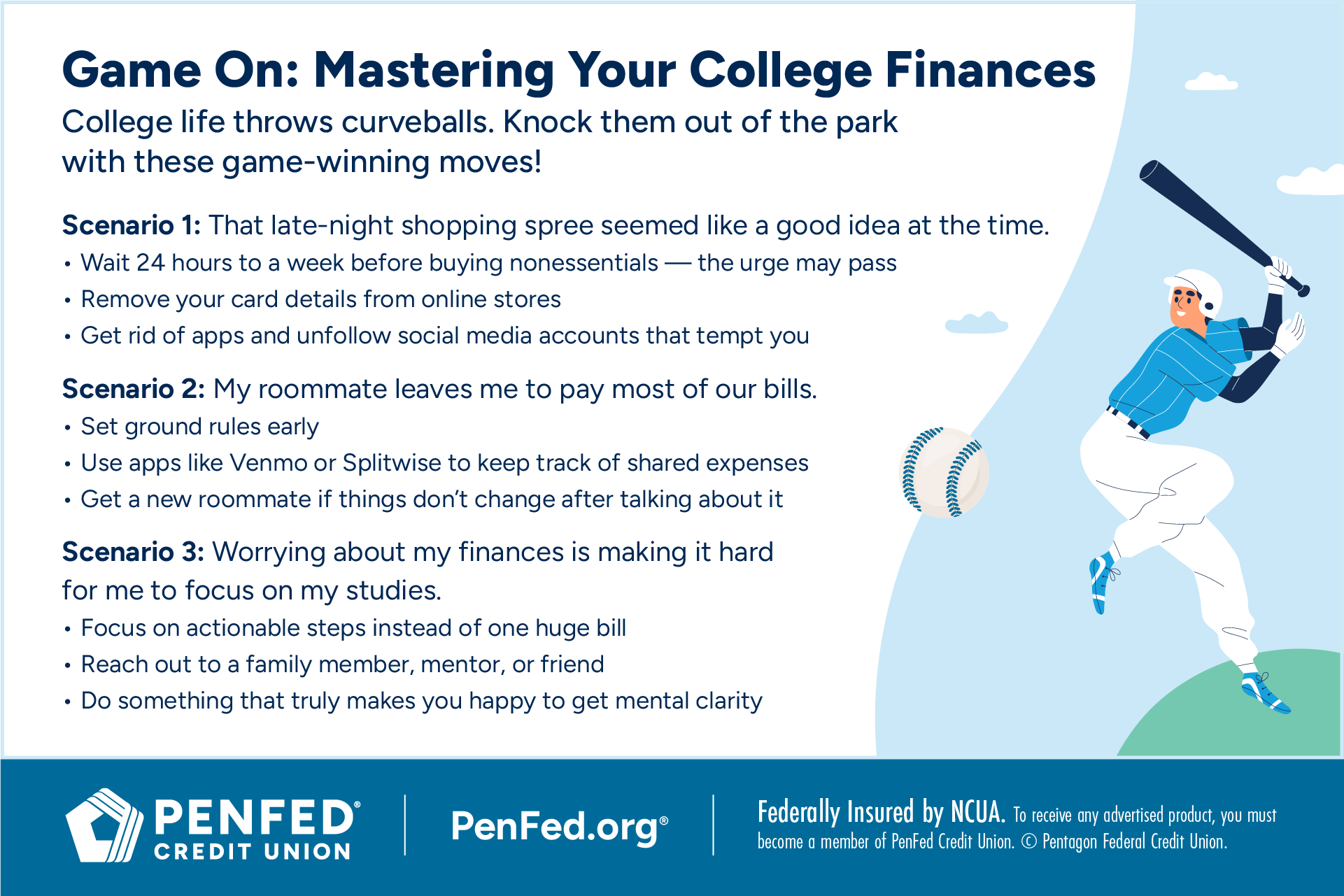

Unexpected expenses: Just like a surprise exam, unexpected costs can hit hard. Maybe your laptop crashes right before finals, you need a next-day flight home, you end up with a flat tire, or a medical bill pops up. Work over the summer and build up your emergency fund so these curveballs don’t send your budget spiraling and tempt you toward high-interest debt.

Social spending: College life is about making connections, and often, that involves spending money — grabbing coffee, dinner celebrations, going to concerts, or weekend trips. The desire to fit in and grow relationships might push you to overspend on social activities. Avoid this trap with loud budgeting and low-cost gatherings. More on that later.

Limited income: If you’re a full-time student, athlete, or non-traditional learner juggling multiple responsibilities, finding time for a part-time job might be a struggle. Few to no work hours means a volatile income, which can make it harder to cover daily expenses. So, what’s the solution? Get creative with your passive income. Instead of long retail or hosting shifts, try lower-lift gigs like tutoring, dog walking, selling digital products, dropshipping, affiliate marketing, and good old investing.

Instead of long retail or hosting shifts, try lower-lift gigs like tutoring, dog walking, selling digital products, dropshipping, affiliate marketing, and good old investing.

Textbook and supply shock: Even after budgeting, the sheer price of textbooks, labs, study supplies, and special software can be a rude awakening. These aren’t just minor purchases — they can be hundreds of dollars per semester. Save some money by renting a textbook and looking for student discounts on tech essentials.

Impulse buys and online shopping: With the convenience of online shopping and delivery apps, it’s incredibly easy to make impulse purchases. Repeat orders of that Chinese takeout or nice-to-have gadget can drain your funds, like tiny leaks in a bucket. So can the subscriptions you don’t use. Do away with temptation by limiting your screen time and app selection. Or commit to a week-long no-spend challenge.

Financial aid shortfalls or delays: Sometimes, financial aid packages don’t cover everything or disbursements are delayed, leaving students in a temporary bind. This is what your emergency fund is for. Bonus tip — it’s always a good idea to apply for as many scholarships and grants as you can.

Think of your budget as a GPS. It shows you where you are, where you want to go, and how to get there.

Create a Budget and Track Expenses

Think of your budget as a GPS. It shows you where you are, where you want to go, and how to get there.

The Basics of Budgeting

Your budget needs to be realistic — and it won’t be like anyone else’s. The goal isn’t to restrict yourself so tight that you cheat yourself out of living.

Start by listing all your sources of income. This might include scholarships, grants, job earnings, or contributions from family. For example, if your parents give you a monthly allowance of $200, and you work a part-time job earning $400 bi-weekly, your total monthly income would be $1,000.

Next, list all your expenses. Think about tuition, housing, food, books, personal care items, transportation, and entertainment.

Then, categorize them into needs and wants.

How to Use the 50/30/20 Rule

Once you’ve figured out the things that are essential and those that you desire but can live without, it’s time to decide how much of your monthly income goes where. The 50/30/20 rule is a great starting point for college students.

It’s straightforward. Simply allocate:

- 50% for needs

- 30% for wants

- 20% for savings and debt repayment

While it’s the smallest slice of the pie, the last bucket is crucial. Saving is how you build your emergency fund and achieve personal goals like putting a down payment on a new car, funding a study abroad trip, or completing professional certifications.

And if you don’t have credit card debt, think about using some of those stashed funds to pay off your student loans. Getting a head start on repayment could mean paying less interest over the life of the loan.

Another effective and easy-to-use strategy is the zero-based budget. Each month, you’ll assign all your income to either expenses and/or savings so that you don’t end up with cash that’s unaccounted for.

Whatever method you choose, make sure it’s something you can stick to.

Even saving $10 a week counts — it could become $520 in a year. Aim for at least $500 to $1,000 to cover minor emergencies.

Building Your Emergency Fund

These three tips are your key to building and maintaining your emergency fund:

Start small: Even saving $10 a week counts — it could become $520 in a year. Aim for at least $500 to $1,000 to cover minor emergencies.

Use a separate account: Keep your emergency fund in a separate savings account, ideally one that’s linked to your checking but not easily accessible for everyday spending. This makes it harder to dip into it for non-emergencies.

Set it and forget it: Set up automatic transfers from your checking to your savings account each payday.

Tools and Apps for Expense Tracking

Spreadsheet, budget planner, or personal finance app — take your pick! The most important thing is that you’re logging every charge you make.

Apps tend to be the go-to because of their convenience and because many students already have experience using them. With round-the-clock accessibility and personalized insights, you can stay in the loop without having to do complex math.

Let’s say you budgeted $100 for entertainment this month and you only spent $75 on brunch. The app will tell you that you’re under your budget. At that point, you can transfer the surplus to your savings or use it for next month’s fun.

Your banking app can also tell you where you stand. It’s usually connected to your checking account. When opening an account, look for student-friendly options with:

- No monthly fees

- Low or no minimum balance requirements

- ·ATM fee reimbursement

Having enough funds for a night out with friends or an occasional coffee with your study group gives you a chance to let off a little steam.

Make and Save Money

We’ve briefly touched on employment and savings. Let’s dig a little deeper.

How to Make Money in College

If your course load allows it, consider part-time work. You may be able to find a work-study job on campus or off-campus roles like a barista, restaurant host, fitness trainer, babysitter, or rideshare driver.

Having your own source of income can help give you more financial freedom when it comes to room and board. If living expenses are good to go, then you can use your paycheck for outings with friends and that cold brew craving without charging it all to your credit card.

If you’re the entrepreneurial type, get a side hustle going. The beauty of a side hustle is that you can pretty much do anything you’re good at. So, tap into your creative talents or unique skills! For example, you can sell handmade goods such as jewelry or holiday themed gifts, refurbish thrifted furniture, design websites, sell T-shirts, or secure a couple freelance writing gigs.

Next on the list is internships. While several of them are unpaid, some offer stipends or hourly wages. Earn some cash and gain real-world experience — it’s a win-win!

While working your way through college is a great way to establish lifelong financial habits, it’s also about the little things. Having enough funds for a night out with friends or an occasional coffee with your study group gives you a chance to let off a little steam and clear your head. And when you have that, you’ll think more creatively and probably retain more of what you learn in class.

Once you’ve signed up for a meal plan, use it. Having a prepaid plan can help you save on groceries or dining out.

How to Save Money in College

Small actions can add up when it comes to saving. Here are five tips to reduce unnecessary expenses.

1. Look for Deals on Textbooks and Supplies

Before paying full price, check these options:

- Buy used

- Rent from an online platform

- Get a digital version for less

- Check your university or local library

- Connect with upperclassmen donating their books

And stock up during back-to-school sales even if you’re heading off to college later in the year.

2. Feed Your Savings, Not Your Cravings

Skeptical about the school cafeteria? Understandable, but meal plans have come a long way. If you have certain dietary needs, investigate what kind of accommodations your school’s dining hall provides. And if you’re still scoping out schools, look for those that offer meals plans that fit your diet and lifestyle, such as vegetarian, vegan, and gluten-free dining options.

Once you’ve signed up for a meal plan, use it. Having a prepaid plan can help you save on groceries or dining out. If permitted, pack snacks or take fruit from the dining hall.

For off-campus students:

- Create a meal plan of your own

- Buy ingredients in bulk when it makes sense

- Look for sales at grocery stores

- Learn to cook basic, low-cost meals

- Share grocery costs and cooking duties with friends and roommates

Always ask if there’s a student discount. Many museums, movie theaters, restaurants, gyms, insurers, cell phone plan providers, airlines, and online retailers offer them.

3. Get Smart About Transportation

Use these cost-effective ways to get from point A to B:

- Walk or bike

- Explore local bus/train routes and get a discounted public transit pass for students

- Use ridesharing apps only for emergencies and special occasions

- Consider carpooling for long trips

- Think twice about bringing a car — no vehicle means no parking fees and refuels

4. Be Strategic About Your Social Life

Have fun without breaking the bank:

- Attend free or low-cost campus events like concerts, movie screenings, sports tournaments, and guest discussions

- Organize potlucks or game nights instead of expensive nights out

- Explore local parks, hiking trails, or beaches — nature is a great escape

- Check out free cultural events, museums, and other happenings in your city

5. Leverage Student Discounts

Always ask if there’s a student discount. Many museums, movie theaters, restaurants, gyms, insurers, cell phone plan providers, airlines, and online retailers offer them.

Setting Financial Goals During College

Maybe you want to save for a spring break trip with friends, upgrade your laptop, or boost your investment account. Whatever your goals, break them down into clear, measurable steps like saving $500 by the end of a semester or contributing $25 to savings each week to make them real and achievable.

Build Credit Wisely

Credit cards can be a double-edged sword for new college students. When used wisely, they can help you build a strong credit history. Plus, some offer perks like cash back, points, and miles on everyday purchases. But when used carelessly, they can lead to debt, which 48% of Americans have.

Do your future post-grad self a big favor and find out all there is to know about credit cards, so you don’t get stuck with overwhelming debt. The peace of mind that comes with a manageable credit card balance, plus a credit score that allows you to rent an apartment, buy a new set of wheels, or get a reasonable mortgage is something you want.

Understanding Credit Cards and Interest Rates

When you’re shuffling from class to work and back, it’s tempting to charge everyday expenses to your credit card. But this can escalate your debt.

Then, there’s interest, which comes into the picture when you don’t pay your balance in full by the due date. It’s like renting a video game or car — if you return it late, you pay an extra daily fee.

Want to know how much interest you might owe? When applying for a card, look at the annual percentage rate (APR) and find out if it’s subject to change based on market conditions. Most are.

One card is enough. You don’t need multiple cards to start building credit. Focus on managing one responsibly.

Tips for Building a Good Credit Score in College

Thinking of getting your first credit card? Here’s what to keep in mind when choosing:

- Start small: Consider a secured or student credit card with a low credit limit.

- One card is enough: You don’t need multiple cards to start building credit. Focus on managing one responsibly.

- Pay on time: This is the golden rule of credit cards. Consistent, on-time payments helps boost your credit score. Set up automatic payments or reminders so you never miss a due date.

- Pay in full, every month: It’s not the end of the world if you can’t pay off your balance in full but just know that interest charges will pile up. Have a plan to tackle that.

- Keep balances low: A credit card is not free money. Treat it like cash in your wallet. Try to use only a small portion of your available credit — best practice is 30% or less. So, if your credit limit is $500, your balance should be at or below $150.

- Monitor your credit score: You can get free annual credit reports from AnnualCreditReport.com.

Bonus tip: Consider reserving your card’s points for a specific category of expenses that might not otherwise fit into a college budget, like a birthday gift for a friend or loved one.

Keeping Your Credit Safe

The world of credit has its traps, and unfortunately, college students are often targets. Being proactive is your best defense against identity theft and financial loss.

- Protect your personal information: Never share your Social Security number, bank account details, or credit card information unless you’re absolutely sure it’s a legitimate source.

- Beware of too-good-to-be-true offers: If an email promises a scholarship for a small fee, debt relief, or you get a text with a link to apply for a credit card, it’s likely a scam. Your university or lender will communicate through official channels.

- Strong passwords: Use unique, strong passwords for all your online accounts and consider two-factor authentication.

- Shred documents: Don’t just toss financial statements or credit card offers in the trash. Shred them to prevent dumpster diving identity thieves.

- Monitor your accounts: Regularly check your bank and credit card statements for suspicious activity. If you see something, report it immediately.

It’s tempting to take out the maximum amount, but every dollar you borrow is a dollar you’ll have to repay with interest. Be as conservative as possible.

Manage Your Student Loans and Financial Aid

The moment you decided on college, the search for student loans began. For many, student loans are a common way to cover college costs, especially when other forms of financial aid only get you so far. However, they come with a significant responsibility — repayment.

Let’s look at why and when a student loan may be right for you, plus how to make the most of it.

Different Types of Student Loans Explained

Knowing the basics of different types of loans is the first step to borrowing wisely. Here’s a simple breakdown:

|

Loan Type |

Who Offers It? |

Interest |

Top Perks |

Things to Watch Out For |

|---|---|---|---|---|

|

Subsidized |

Dept of Ed |

Yes (the government pays) |

The government covers interest while you’re in school and during grace periods. |

Only for undergrad students with demonstrated financial need. Borrowing limits apply. |

|

Unsubsidized |

Dept of Ed |

Yes (you pay) |

Available to all students regardless of financial need. |

Interest adds up while you’re studying, making the total cost higher. |

|

PLUS |

Dept of Ed |

Yes (you pay) |

For parents of undergrads and for graduate/professional students. Can have higher borrowing limits. |

May have higher interest rates than other federal loans. A credit check is required. |

|

Private |

Banks, credit unions, and other lenders |

Yes (you pay) |

Can cover gaps when federal aid isn’t enough. |

Often have high interest rates, limited repayment flexibility, and usually require a co-signer. |

The key here is to always maximize federal loans first before considering ones from private lenders. That’s because federal loans generally offer more protections, flexible repayment plans, and sometimes, lower interest rates.

How to Effectively Manage Student Loan Repayments

Owing money, especially such a large amount, might spook you a bit. Beat anxiety and get smart about repayment with these seven tips:

- Borrow only what you need: It’s tempting to take out the maximum amount, but every dollar you borrow is a dollar you’ll have to repay with interest. Be as conservative as possible.

- Know your repayment terms: Understand when repayment begins (usually after you graduate or drop below half-time enrollment) and interest rates. Study the fine print.

- Choose a repayment plan: There are various repayment plans, including income-driven options. See what works for you.

- Automate payments: Set up automatic payments like you would with your credit card.

- Keep track of your loans: Use a spreadsheet or online tool to track all your loan balances, interest rates, and payment dates.

- Consider interest payments while in school: If you have unsubsidized loans, interest accrues while you’re in school and you’re expected to pick up the tab. Paying even small amounts during college can save you a lot in the long run.

- Communicate with your lender: Life does its thing. If you find yourself in a pickle, reach out to your loan servicer right away to discuss your options.

Leveraging Financial Aid and Scholarships

Student loans are helpful, no doubt. But what if there were financial aid options that you didn’t have to pay back? Game-changing, right? Think of scholarships and grants as free money that reduces your reliance on loans.

- Grants: These are typically needs-based. They’re like a gift from the university, state, or federal government. The Free Application for Federal Student Aid (FAFSA) is your gateway to federal grants like the Pell Grant.

- Scholarships: These are often merit-based, recognizing achievements in academics, athletics, leadership, and more. The world of scholarships is vast and there are opportunities for almost everyone.

Strategies for Finding and Maximizing Aid

- FAFSA is your first step: Don’t think of FAFSA as a one-and-done task. You need to fill it out annually to re-evaluate your eligibility for federal, state, and even some institutional aid. Missing the deadline can mean missing out on valuable funds.

- Explore local avenues: Find out from your high school guidance counselor, local nonprofits, and civic groups what scholarships are available for students in your area. These can be less competitive than national awards.

- Tap into your university’s resources: Your college’s financial aid office can tell you all about institutional scholarships, departmental awards, and special programs. Schedule an appointment and ask questions.

- Dig into online scholarship databases: Websites like Scholarships.com and Collegeboard.org are powerful tools in your search. Be specific with what you’re looking for.

- Make your application compelling: Don’t just fill out the blanks or copy and paste across applications. Personalize your essays, highlight your unique strengths, and proofread everything. A well-written application stands out, much like a shining résumé.

- Put in several applications: The more applications you fill out, the greater your chances of securing multiple aid packages.

- Keep looking after freshman year: Many students stop searching for scholarships after their first year, but opportunities are available throughout your entire college career.

Finally, securing a scholarship or grant can feel like winning the lottery, but this money is purpose-driven. Prioritize tuition and other essentials and say no to extravagant items.

Develop Long-Term Financial Habits

Your college years fly by, and before you know it, you’ll be walking across that stage. Thinking about your finances now isn’t just for today — you’re laying the groundwork for a healthy financial life after the cap toss.

Leverage What You’ve Learned at Home

College is a great time to put your family’s money lessons to use. Maybe you practiced strict budgeting using envelopes, you consistently recited money mantras, or your family was all about having a business mindset. Lean into the good and come up with money values of your own along the way.

Preparing for Post-College Financial Success

Start thinking about your career path now. Research potential earnings, visit your college’s career services office, and talk to alumni and professionals. Get your feet wet with an internship and continuously seek opportunities to learn new skills. The more transferrable and in-demand skills you have, the more marketable you become.

All this combined with smart saving and spending will land you right where you need to be.

Get your feet wet with an internship and continuously seek opportunities to learn new skills.

The Takeaway

Congratulations on taking a step to better your education! As you crush your academic goals, don’t forget to study up on different tools, resources, and methods for developing sound personal finance habits that fit your lifestyle. Not only will finding the right approach help you determine the right amount of money to have before going to college, but it can also help you stay on track toward your goals while in school, so you get to the financially secure future you’ve always dreamed of.

Invest in Your Future

Get a PenFed loan to fund your studies, from start to finish.