STUDENT LOANS

Federal vs. Private Student Loans: What’s the Difference?

EXPECTED READ TIME: 10 MINUTES

Paying for post-secondary education (aka college tuition) isn't easy. Whether you're heading to a university, technical college, or trade school, you'll have to cover expenses that likely exceed your budget.

If you're considering using student loans to help cover these costs, then you might be wondering whether you should use federal vs. private student loans. In most cases, students should apply for federal student loans first because the terms are usually better. However, there are some cases where private student loans can be a good choice.

What Are Federal Student Loans?

Federal student loans are made to students by the U.S. Department of Education. These loans are intended to cover the cost of tuition and fees, books, housing, food, and transportation. Eligible students can apply for federal student loans by completing the Free Application for Federal Student Aid, or FAFSA, which determines the types of financial assistance they qualify for. (In addition to federal student loans, some applicants may qualify for grants or work study programs by completing the FAFSA.)

Types of Federal Student Loans

The U.S. Department of Education offers four types of student loans. Which loans you qualify for depends mainly on your degree of financial need and whether you already carry any federal student loan debt.

Direct Subsidized Loans

Direct Subsidized Loans are available to undergraduate students who demonstrate financial need. Your financial need is based on the cost of your school minus your expected family contribution and any other financial assistance you've received (like scholarships or grants).

Subsidized loans also have the lowest origination fees of any federal student loan.

With direct subsidized loans, the U.S. Department of Education pays interest on the loan for you in a handful of scenarios, such as:

- While you're in school

- For the first six months after graduation

- During any periods of deferment (temporary breaks from payment, usually due to emergency situations like job loss)

Direct Unsubsidized Loans

Direct unsubsidized loans are available to all undergraduate and graduate students who qualify for federal student loans. Your eligibility is not based on financial need or your credit report.

With direct unsubsidized loans, you are responsible for paying the loan's interest. If you choose not to pay this interest while you're in school and during the first six months after graduation, that interest will build up and be added to the principle of your loan once you start paying again.

Direct PLUS Loans

Sometimes these are known as "graduate PLUS loans" or "parent PLUS loans." You do not have to demonstrate financial need to be eligible for PLUS loans, but you will be subject to a credit check. If you have poor credit, you may have to meet additional requirements — like credit counseling— before you are eligible for a PLUS loan.

Direct PLUS loans are available for:

- Graduate students

- Professional students

- Parents of dependent undergraduate students

PLUS loans also carry the highest fees of any federal student loans. Unlike with subsidized and unsubsidized loans, you are responsible for paying the interest on PLUS loans right away unless you formally request a deferment. Interest will continue to build and be added to the principle of your loan throughout periods of deferment.

Because the terms on these loans are less favorable, borrowers usually only turn to PLUS loans once they have borrowed the maximum amount available in subsidized or unsubsidized loans.

Unlike with subsidized and unsubsidized loans, you are responsible for paying the interest on PLUS loans right away.

Direct Consolidation Loans

Direct consolidation loans offer students a way to combine multiple student loans into one loan with a fixed interest rate that's ideally less than the rate on your previous loans. Plus, it means only one student loan bill per month instead of multiple bills with different due dates. Not a bad deal!

In addition to direct consolidation loans, borrowers also have the option of refinancing student loans through private lenders such as banks and credit unions. Like with debt consolidation, refinancing can land you lower interest rates or smaller monthly payments that make paying off your debt more manageable.

What Are Private Student Loans?

Private student loans are made to students by nonfederal lenders such as banks, credit unions, nonprofits, or schools themselves. Like federal student loans, private student loans cover expenses related to school.

The major difference between federal and private student loans is that private student loans are issued by private lenders who set the terms for their loans, so terms may vary from one lender to another. Most private lenders are for-profit lenders, meaning they loan money with the purpose of making a profit from interest and other charges on the loan. However, some nonprofit private lenders do exist.

Most private lenders are for-profit lenders, meaning they loan money with the purpose of making a profit from interest and other charges on the loan.

Differences Between Federal and Private Student Loans

There are a number of important differences between federal and private student loans. When it comes to paying back your loans, these differences can mean paying thousands of dollars more (or less) depending on the type of lender and loan you go with. For that reason, it's important you know how eligibility, interest rates, repayment plans, and grace periods work for both types of loans.

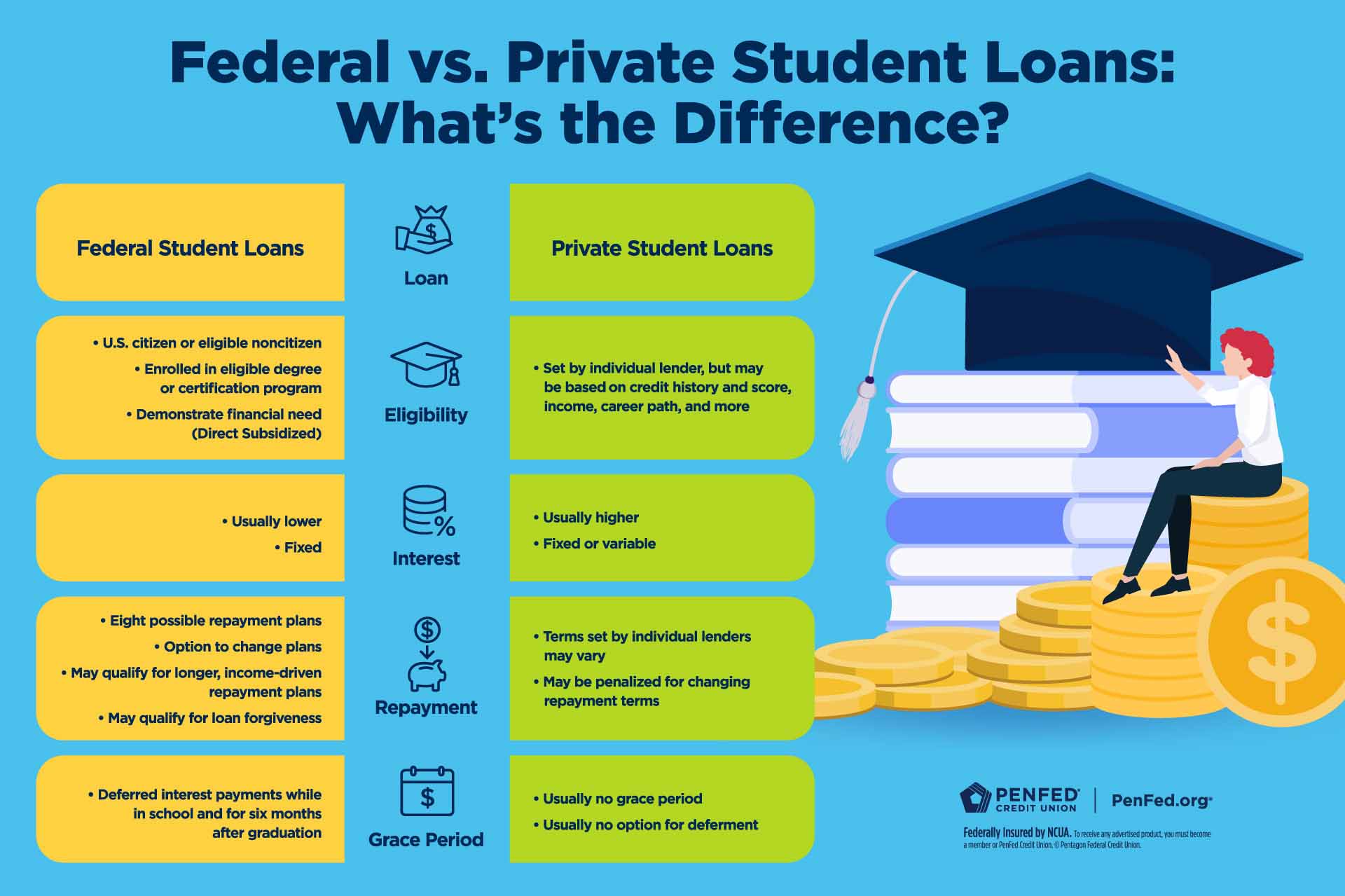

Eligibility Requirements

Qualifying for federal student loans is straightforward. The basic requirements dictate that you must:

- Be a U.S. citizen or eligible noncitizen

- Be enrolled in an eligible degree or certificate program

- Demonstrate financial need (find the complete criteria for eligibility here)

Qualifying for a private student loan is more complicated. Like with any loan, your lender will evaluate your creditworthiness before issuing a loan. That means the lender will consider factors such as your:

- Credit score

- Credit history

- Income

- Work history

- Any other debt you have

Some lenders also consider your major, the career you plan to enter after graduation, and the cost of your school. If you receive a private student loan and any of these factors change while you are in school, those changes may affect the terms of your loan.

In addition to loans, look for other forms of financial aid that don't need to be repaid, like grants, scholarships, and employee educational benefits.

Interest Rates

Federal student loans usually come with lower interest rates because they are backed by the federal government. The U.S. Department of Education acts like a nonprofit lender. Even though federal loan borrowers do pay interest, this interest is rolled back into the government's lending program to fund loans for future borrowers.

In contrast, private lenders loan money to students for profit, making money through interest charges and fees on loans. Private lenders also charge higher interest because they assume a greater risk when lending money than the Department of Education does.

In addition to offering lower interest rates, federal student loans come with fixed interest rates. This means that even if interest rates rise, your student loan's interest rate will remain the same. With private lenders, your interest rate can be fixed or variable depending on the terms you negotiate. If you have a variable interest rate and interest rates rise, you may end up paying more for your loans than you expected.

Importantly, many private lenders set minimum monthly payments that are not high enough to cover a loan's monthly interest charges, so making minimum monthly payments on a private student loan may not be enough to pay it off. In the case of federal student loans, each monthly payment includes money toward the principle and the interest for that loan.

Repayment Plans

When it comes to repayment options, many borrowers choose federal student loans because of their flexible repayment plans. The Standard Plan is the default — if you make your minimum required payment every month, you'll pay off your loan in 10 years.

However, other repayment plans exist that may be better in some circumstances, especially if a crisis arises. For instance, the U.S. Department of Education offers a series of income-driven repayment plans where a borrower's monthly minimum payment is tied to their income. This way, a borrower's monthly payments will never exceed more than 10% of their discretionary income. (Discretionary income is the amount of money left over after you pay for essentials like food and rent.) Another option is the graduated repayment plan, which starts with much lower monthly payments that increase every two years.

Making minimum monthly payments on a private student loan may not be enough to pay it off.

With private student loans, your individual lender will set the terms for repayment. It's possible a private lender may offer you better student loan terms under the following conditions:

- You only borrow a small amount

- You put up collateral for your loan (otherwise known as a secured loan)

- You have excellent credit

- You have a cosigner

But most students are looking to borrow large amounts with no collateral and little credit, so they receive less desirable terms.

Private lenders may also be willing to renegotiate your terms similar to the way federal student loan borrowers can switch between repayment plans, but this is entirely up to the private lender. Even if your lender does agree to renegotiate, you may incur additional fees if you alter the terms of your loan.

Grace Period for Repayment

Another big difference between repaying federal student loans and repaying private student loans is that borrowers do not have to begin repaying their federal student loans until six months after graduation. This grace period is designed to give borrowers time to find work and build wealth before they begin making loan payments. On the other hand, most private lenders require you to begin paying as soon as you graduate. Some even require payments while you're still in school completing your degree.

The Takeaway

So, which student loan is right for you? When you're ready to apply for student loans, we suggest starting with federal loans. Their lower interest rates and flexible repayment plans make them a better deal for most students. However, there are times when private student loans can be helpful. If your school costs more than the maximum amount you can borrow in federal loan money, then you might supplement your federal borrowing with private loans if the interest rate for those private loans is lower than the interest rate on federal PLUS loans. Private student loans can also be a good option for those who don't qualify for federal student loans.

In addition to loans, look for forms of financial aid that don't need to be repaid, like grants, scholarships, and employee educational benefits. You can find more information about free college funds through your high school guidance office, college financial aid office, local public library, or free online scholarship websites.

Ready to Finance the School of Your Dreams?

Discover the diverse offering of products, services, and support available to our members.