STUDENT LOANS

Federal Student Loans Explained: Subsidized vs. Unsubsidized

What You’ll Learn:

The differences between subsidized and unsubsidized federal student loans.

Expected Read Time: 5 Minutes

Federal student loans fall under two broad categories: subsidized and unsubsidized.

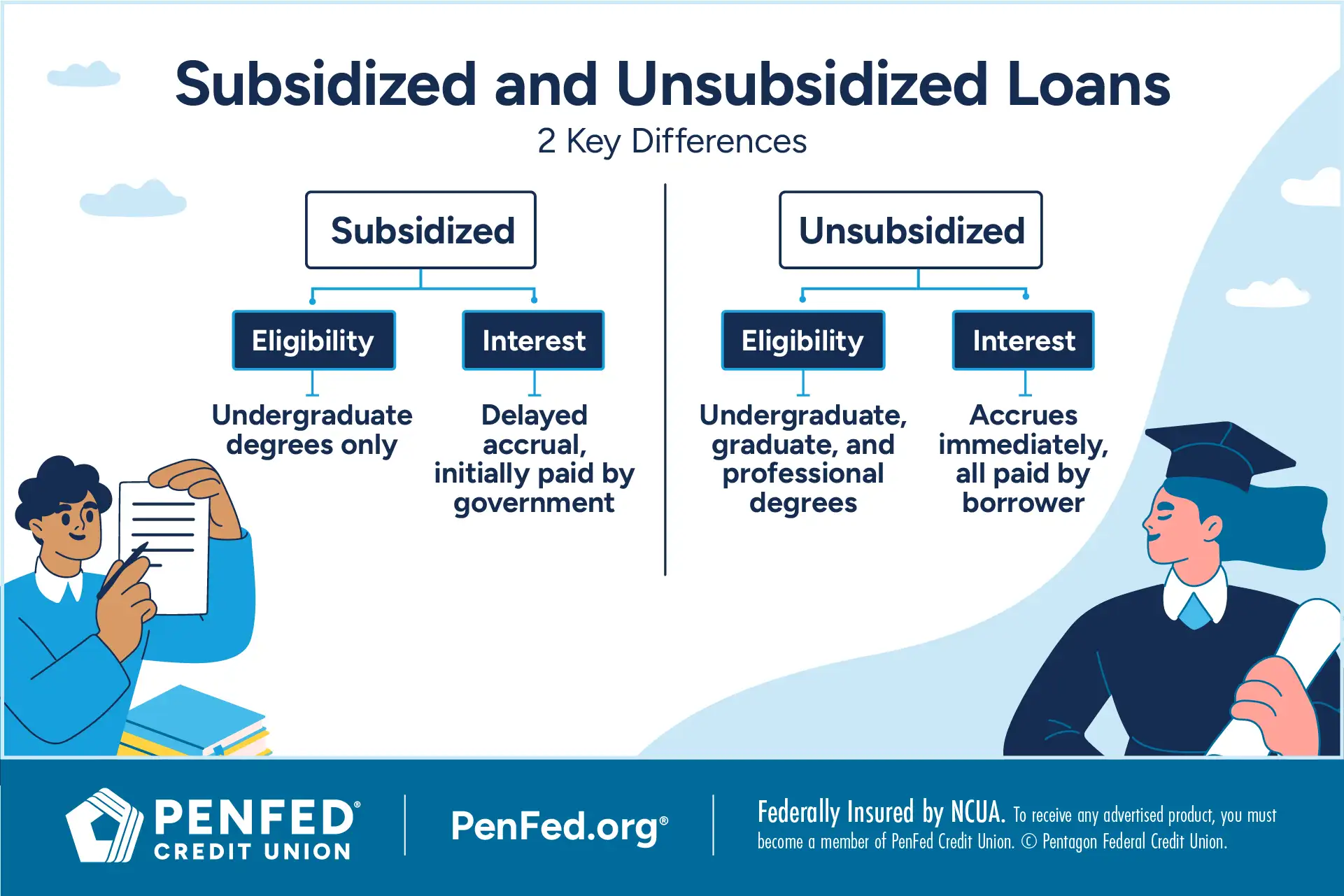

Subsidized student loans:

- Need‑based

- Undergraduate students only

- Government pays interest during school and during a 6‑month grace period

- Save money in the long term vs. unsubsidized

Unsubsidized student loans:

- Broader eligibility (not need-based)

- Undergraduate, graduate, and professional students

- Borrower pays all interest, which accrues from disbursement

- Broader eligibility vs. subsidized

What Is a Subsidized Loan?

A subsidized loan — officially known as a direct subsidized loan — is a type of federal student loan available to undergrads who demonstrate financial need. These fixed-rate loans, which are offered by the U.S. Department of Education, can be used to help pay for higher education costs at a four-year college or university, community college, or technical school.

What Is an Unsubsidized Loan?

An unsubsidized loan — formally known as a direct unsubsidized loan — is a form of federal student loan available to both undergraduate and graduate students who meet the requirements for federal student aid. Unlike with subsidized loans, eligibility for unsubsidized loans isn’t determined by financial need.

Eligibility for unsubsidized loans isn’t determined by financial need.

What Are the Differences Between Subsidized and Unsubsidized Loans?

Both subsidized and unsubsidized student loans are low-interest loans offered by the federal government to pay for post-secondary education. Neither type of student loan requires a credit check, and both offer more repayment options than private student loans.

Despite the similarities, there are key differences between subsidized and unsubsidized student loans. They include:

Eligibility

Subsidized loans are only available to undergraduate students who can show financial need. You can estimate your financial need by subtracting the amount of money you have saved toward tuition — also known as your expected family contribution (EFC), and any other financial assistance you receive, like scholarships or grants — from the total cost of attendance.

Unsubsidized loans, on the other hand, are open to undergraduate, graduate, and professional degree students. You only need to meet basic student loan eligibility requirements to qualify for an unsubsidized loan.

Interest

With a subsidized loan, the Department of Education pays (or “subsidizes”) the loan interest while you’re enrolled in school at least half-time and for a six-month grace period after you graduate. Payments on subsidized loans can also be deferred in certain situations.

Meanwhile, with an unsubsidized loan, interest charges begin to accrue from day one. You’re also responsible for paying any interest that accumulates while you’re in school and throughout the life of the loan, even during periods of deferment.

Although interest is paid back differently with subsidized and unsubsidized loans, the government charges the same interest rate for both types of loans — for undergrads, that is. Graduate-level or professional degree students are charged higher rates than undergraduates for unsubsidized loans.

The government charges the same interest rate for both types of loans — for undergrads, that is.

Loan Limits

Subsidized and unsubsidized loans have annual and total lending limits that vary widely. The exact amount depends on your year in school and whether you’re a dependent (someone else can claim you on their income tax returns) or an independent student.

For example, if you’re a dependent undergraduate student, the maximum amount you could borrow with federal student loans are as follows:

- First year limit: $5,500, with subsidized loans capped at $3,500

- Second year limit: $6,500, with subsidized loans capped at $4,500

- Third year and beyond limit: $7,500, with subsidized loans capped at $5,500

- Total limit: $31,000, with the total of subsidized loans capped at $23,000

On the other hand, if you’re an independent undergraduate student, you could potentially borrow up to the following amounts in combined subsidized and unsubsidized loans:

- First year limit: $9,500, with subsidized loans capped at $3,500

- Second year limit: $10,500, with subsidized loans capped at $4,500

- Third year and beyond limit: $12,500, with subsidized loans capped at $5,500

- Total limit: $57,500, with the total of subsidized loans capped at $23,000

It’s worth noting that the total amount of a subsidized loan can’t exceed your demonstrated financial need.

As a graduate or professional student, you can borrow a maximum of $138,500 in total federal funds, including both subsidized and unsubsidized. Keep in mind that the aggregate limit includes federal loans for undergraduate study, and no more than $65,500 of the combined total graduate/professional and undergraduate can be in subsidized loans.

The total amount of a subsidized loan can’t exceed your demonstrated financial need.

Yet in the end, the school you attend will determine how much you can borrow with either type of loan using information in your Free Application for Federal Student Aid (FAFSA) form.

What Are the Pros and Cons of Subsidized vs. Unsubsidized Loans?

Still not sure if a subsidized or unsubsidized loan is right for you? Here’s a snapshot of pros and cons to help you decide.

|

Subsidized Loan |

Unsubsidized Loans |

|---|---|

|

Government pays interest while enrolled |

Borrower pays all interest charges over life of the loan |

|

Eligibility based on financial need |

Not contingent upon financial need |

|

Single-digit, fixed rates |

Higher interest rates for graduate students |

|

Available only to undergraduate students |

Available to undergraduate, graduate, and professional students |

|

Interest doesn’t accrue until after graduation |

Interest begins to accrue immediately |

|

Lower lending limits |

Higher lending limits |

Is It Better to Have a Subsidized or Unsubsidized Loan?

Strictly speaking, a subsidized loan is better than an unsubsidized loan. With a subsidized loan, interest doesn’t start to accrue until after you graduate, which means you’ll save money over the life of the loan.

Strictly speaking, a subsidized loan is better than an unsubsidized loan.

Of course, depending on your financial situation, you may not qualify for a subsidized loan. In that case, you’re still better off applying for an unsubsidized loan before turning to private loans that charge higher interest rates (the repayment options may not be as flexible either).

The Takeaway

Used wisely, a subsidized or unsubsidized student loan provides a great way to finance some or all of your post-secondary education. So, do your research, understand your options, and choose the path that will help turn your dream into a reality.

Explore Student Loan Options at PenFed

Discover the diverse offering of products, services, and support available to our members.