CREDIT CARDS

How to Pay Off Credit Card Debt

What you'll learn: How credit card affects you and how to pay it off

EXPECTED READ TIME: 9 MINUTES

Credit card debt is pretty common. In fact, over half of Americans have outstanding balances on their credit card.

While some debt can be beneficial, too much debt can be stressful and keep you from meeting important financial goals like saving for college or investing for retirement. Credit cards in particular tend to be expensive, with higher interest rates than personal and home equity loans.

Yet many people find themselves on a carousel of paying down debt only to charge more. If that sounds familiar, PenFed is here with tips rein in your credit card debt once and for all.

Understanding Credit Card Debt

Credit card debt is tough to pay down because it’s expensive and revolving. Since most credit cards are unsecured, they come with higher interest rates that can grow your balance quickly.

You can also keep spending with your card as long as you make minimum payments each month, so while it may feel like you’re paying off your debt, you’re actually caught in a cycle of spending and repayment.

Causes of Credit Card Debt

In some cases, people end up in credit card debt as a result of financial emergencies. Ill health, job loss, car accidents — any unavoidable, expensive event can push people to rack up big balances. Then interest kicks in and makes it hard to pay down that balance.

Other times people end up with credit card debt as a result of overspending or spending beyond their means. It’s easy to use your credit card to split up big purchases or cover a purchase until payday rolls around — but do that too often and your expenses can outgrow your paycheck.

Eliminating any kind of debt puts you in a safer financial position.

Reasons to Pay Off Your Credit Cards

Paying off your credit card carries big benefits. For one thing, it can improve your credit utilization, boosting your credit score and establishing a healthy payment history.

You’ll also have more money for other things. Whether you’re saving up for a house or preparing for a career change, eliminating credit card debt frees up money for you to do it.

Finally, eliminating any kind of debt puts you in a safer financial position. You’ll be better prepared to manage financial emergencies if you have some extra cash you can draw on instead of turning to credit cards or loans.

If your budget doesn’t match your earning and spending habits, it won’t help you get out — and stay out — of debt.

Creating a Monthly Budget and Setting Debt Payoff Goals

Having a good budget that you can actually follow is foundational to controlling debt. If your budget doesn’t match your earning and spending habits, it won’t help you get out — and stay out — of debt. That’s why the first step in creating a budget is gathering financial documents like pay stubs, receipts, and statements from your credit cards and checking accounts.

Once your budget is set, you can start making realistic goals about how to pay down your debt. It may be tempting to attack that debt aggressively by throwing every spare dollar at it, but don’t skimp on saving. Having a healthy savings account to help with cash flow and an emergency fund to fall back on can prevent backsliding into more debt.

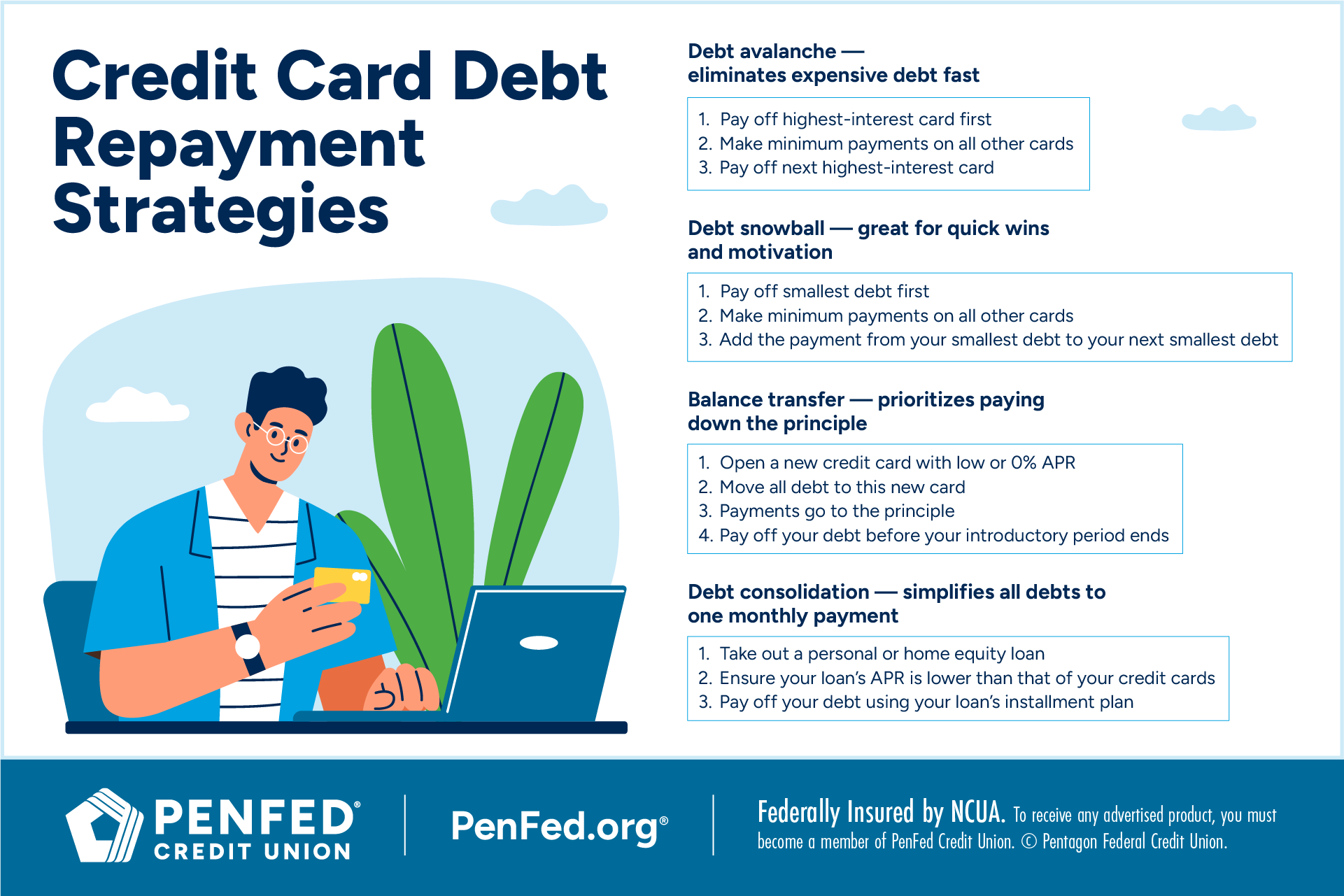

Exploring Debt Repayment Strategies

There are three main strategies for paying off debt. Depending on the amount you owe, the number of cards you’re paying off, and the amount of interest on those cards, some payoff strategies may work better for you than others.

Debt Avalanche

The goal of the debt avalanche method is to pay off the credit card with the highest interest rate first while making minimum payment on all other cards. Once the card with the highest rate is paid off, move onto the card with the next highest rate.

Use the money you would have put on your now paid-off credit card toward your second highest rate card. This way you’ll apply larger and larger payments to the principle of your most expensive card and pay down your debt faster.

The goal of the debt avalanche method is to pay off the credit card with the highest interest rate first.

Debt Snowball

Instead of prioritizing credit cards with the highest interest rates, the debt snowball method focuses on the smallest balance. Start small by making the minimum payment on all credit cards except for the one with the smallest balance. Once that balance reaches zero, take the amount that went toward your first card and apply it to the card with the next lowest balance.

While you may not save as much money in interest as with the avalanche method, this method is highly motivational. Once you’ve scored a win — paying off an entire credit card balance — you’ll feel more confident to continue tackling the rest of your debt. If you’re overwhelmed facing a mountain of credit card debt, the debt snowball method may help.

Once you’ve scored a manageable win, you’ll feel more confident to continue tackling the rest of your debt.

Balance Transfer

The fastest way to pay off your credit card debt is a balance transfer. This is the process of moving debt from one or more credit cards to another card with a lower interest rate. This allows you to put more money toward the principle of your debt. Depending on your credit score, you may qualify for a card with a much lower rate, or even one with an introductory rate as low as 0% APR.

However, this isn’t a cost-free solution. Some issuers charge balance transfer fees, either a flat rate or a percentage of the balance transferred. Make sure that those fees are lower than the amount you’ll save in interest charges or else it may not be worth it.

Before transferring your balance, consider the details: how long the introductory period lasts and what your new card’s rate will be when that period ends. Remember, if you don’t pay off your debt, you’ll be stuck paying the transfer card’s APR, which may be higher than that of your current.

Debt Consolidation Loans

Debt consolidation is the process of combining multiple credit card debts by using a personal loan to pay them off. The main advantage is this simplifies your debt, leaving you with one monthly payment and one APR.

Depending on your loan’s terms, you may be able to lower your monthly payments, pay less in interest, and pay your debt off faster. But read your loan agreement carefully because you could also end up paying more due to fees and interest, especially if your loan term is longer than several months.

Using Your Home’s Equity to Pay Off Credit Card Debt

If you’re struggling to qualify for a great rate on a personal loan, you might consider tapping into your home equity. With your house as collateral, you may land a much lower rate than the average rate of your credit cards, but the trade-off is that you could lose your home if you’re unable to pay off your debt.

To avoid going under with a HELOC (home equity line of credit) or home equity loan, you want to make sure you would be able to pay off what you owe if you had to sell. Usually, home equity loans and lines of credit are based on an appraisal that accounts for your home’s worth. And, depending on your lender, you typically can only borrow up to 90% of your calculated equity.

Just make sure to ask the loan officer to go over in detail what your monthly payment will be if you borrow X amount. Then you can decide if that monthly payment works with your income before taking out the loan. You should also know that HELOCs usually have variable rates, which means your payment could fluctuate slightly.

You might consider tapping into your home equity to pay off high-interest debt.

Managing Expenses and Increasing Income

Regardless of which debt payoff strategy you settle on, you’ll speed up the process if you cut expenses, increase your income, and redirect extra funds to your debt.

Making or revising your budget can help you identify bad spending habits to cut. For instance, are there conveniences you can eliminate such as buying coffee on the way to work, eating out, or having food delivered? Could you clip coupons and use a shopping list to save on groceries? If you struggle to stick to your budget, consider using the envelope system to curb your spending.

Another option is to increase your income. If you can’t do this through a raise at work, consider a side hustle. Freelancing during weekends or evenings can bring in money and diversify your work experience, while a passive income stream could help eventually help cover family vacations or boost your retirement once you’re debt-free.

Seeking Professional Assistance for Credit Card Debt

If you’re feeling overwhelmed by credit card debt, there are ways to get help. It may be time to contact a professional if:

You’re struggling to make minimum payments

Your cards are maxed out

Receiving collection calls

Relying on credit cards to cover daily expenses

Contact Your Lenders

If your debt is the result of difficult circumstances, such as an illness or layoff, contact your lenders and ask if they offer hardship programs. Many lenders offer short-term assistance programs that may reduce your minimum payments or interest rate upon proof of your hardship. Lenders who don’t offer hardship programs may still be willing to negotiate the terms of your debt to help you make your payments.

Many lenders offer short-term assistance programs that may reduce your minimum payments.

Debt Management Plans

Credit counseling agencies, which are also called debt management companies or debt relief services, can help you by negotiating with your creditors to make it easier for you to repay your debt. They can draft a debt management plan designed to help you pay off your credit cards in three to five years.

Once you and your creditors agree to their terms, you’ll start paying the credit counseling agency. The agency will break up your single payment and use it to pay your creditors.

The advantage of a debt management plan is that you don’t need good credit to qualify. Like with other forms of consolidation, it reduces all your debt to one monthly payment. However, it’s important to research agencies carefully to ensure you find one that offers competitive terms without outrageous fees.

The advantage of a debt management plan is that you don’t need good credit to qualify.

Debt Settlement

Debt settlement involves negotiating with your creditors on a settlement for you to pay. This settlement is a lump sum payment that is lower than the amount you actually owe. Some creditors will do this for fast cash and because chasing debt is costly.

But debt settlement isn’t a perfect solution, which is why it’s usually reserved for people facing bankruptcy who are at least 120 days past due. You’ll still need to pay a large sum of money, and the IRS will consider your settlement as taxable income. Additionally, some details related to your settlement may remain in your credit report for up to seven years.

The Takeaway

Often, the key to paying off credit card debt is finding a strategy and sticking to it. Now that you know the options, it’s time to gather up your documents, crunch a few numbers, and chart your path to debt-free financial freedom.

Explore Your Savings Options

Discover the diverse offering of products, services, and support available to our members.