CREDIT CARDS

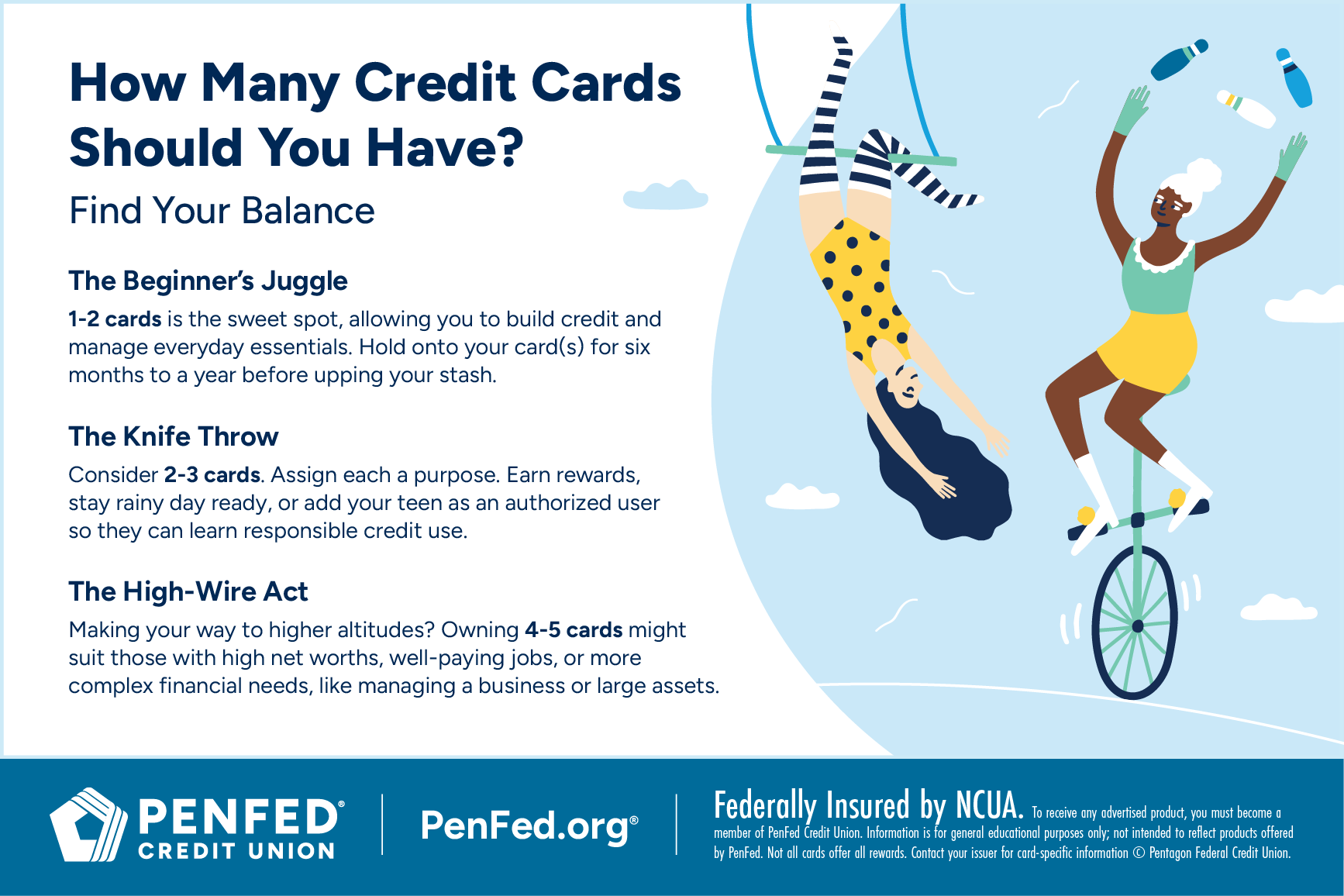

How Many Credit Cards Should I Have?

What you'll learn: How to determine your ideal number of credit cards.

EXPECTED READ TIME:8 minutes

Think of your trusty toolbox. Each tool serves a purpose, from tightening screws on a wobbly shelf to getting the measurements perfect for your new backsplash idea.

Credit cards work similarly. One might be excellent for earning cash back on groceries and gas, another for scoring exclusive discounts at your favorite department store, and a third for unexpected expenses.

But just as a toolbox can get cluttered, having too many credit cards can take a turn for the worst. Too much bad debt across cards can put a dent in your credit score and negatively impact your overall finances.

So, what’s the magic number? Is there such a thing as too many credit cards? The truth is there is no one-size-fits-all answer. Much like a tool collection, the number of cards you own is unique to you and is neither “good” or “bad.” It all comes down to understanding your needs, spending habits, and ability to manage credit responsibly. We’ll walk you through all three of these factors and more, to help you figure out what makes sense for you.

Let’s get started!

Why Get a Credit Card in the First Place?

Credit cards offer tap-and-go convenience on everything from your morning coffee to utility bills. Whether you’re planning a big family vacation or need extra funds to clear your medical dues, the payment flexibility of a credit card makes it possible. It’s no wonder more than 80% of Americans carry at least one in their wallet.

When wielded wisely, credit cards can help you build a strong credit history. Consistent, on-time payments and keeping your spending in check is how you get there. Just remember, more credit cards mean more work. You’ll need to keep up with multiple billing cycles, payment due dates, and maybe even annual fees.

Average Number of Credit Cards

What is the average number of credit cards per U.S. consumer? As of 2023, that number is close to 4 — 3.9, on average. Remember, average doesn’t mean “ideal.” This average includes a wide range of financial situations and aspirations. Some people thrive with just one or two carefully managed cards, while others use more for specific rewards.

Deciding on the Right Number of Cards

Now, on to getting the credit card (or cards). There’s a credit card to match each of the ways you spend and the goals you’re chasing. Additionally, having several cards can be good for budgeting, especially if your income is volatile. It allows you to get specific by mapping out your expenses and matching them to a single source.

The following sections will tell you what matters most when coming up with your golden number. But before that, let’s consider your credit report.

Some people thrive with just one or two carefully managed cards, while others use more for specific rewards.

Credit bureaus often recommend people carry five or more lines of credit. That doesn’t mean you have to have five different credit cards — in fact, a mix of credit is better.

But why five?

Because it makes for a robust profile. Each month, your credit card or loan issuer reports payment activity on your active accounts to the major credit bureaus (Equifax, Experian, and TransUnion). Ultimately, you’re building your payment history five times faster than you would with just one card or line of credit.

Evaluating Your Personal Financial Situation

Whether you’re applying for your first or third card, it’s important to take a good, hard look at your current financial situation. Run some numbers and ask yourself these honest questions:

What is your monthly income and how much do you spend on fixed expenses?

Understanding this flow of money is fundamental. Are you living paycheck to paycheck or do you have a comfortable buffer? Consider all earnings including those from side gigs and company bonuses. Track the ins and outs of your cash with a budgeting app.

Do you have existing debt?

This includes loans and other credit card balances. If you have significant high-interest debt, adding more credit could be risky. As a general rule, your monthly credit card payments should not exceed 10% of your take-home pay. While a new card might seem like it will ease the burden of making ends meet, it could worsen your situation. The exception to this may be a balance transfer credit card, which makes it convenient to pay part or all of your balance thanks to a temporary low-to-zero annual percentage rate (APR). Just be mindful of transfer fees and the promotional period’s end date.

What are your spending habits and what’s your strategy for using each card?

Are you a meticulous budgeter or more of a spontaneous spender? And what are your primary spending categories? Look at past card statements. Your spending style can tell you a lot about how you’ll manage multiple lines of credit. Some people like to shop using cash. Others prefer to use their debit card for everything. There are no interest charges with these methods and you’re less likely to overspend. These kinds of shoppers can easily get by with one or two credit cards for big purchases or emergencies.

However, if you prefer to charge all your expenses and pay off your credit card at the end of the month, then you may need more credit cards to spread out your spending and reap the best rewards. When it comes to emergencies, using your credit card isn’t necessarily a bad idea. If you have to replace a blown-out tire today and you’re sure your next paycheck will cover it, using your credit card makes sense.

Your spending style can tell you a lot about how you’ll manage multiple lines of credit.

How Personal Goals Impact Your Decision

Maybe you’re saving for a down payment on a house, ready to grow your family, or gearing up to start a consulting business. Your goals — both short- and long-term — can help you determine which types of credit cards will be most beneficial to you.

In addition to goals, there are your interests. Do you want to see more of the world? There’s a card for that.

Matching Your Goals and Interests with the Right Cards

Ready to pick from the sea of choices? Start here.

For travel enthusiasts: If you travel often for work or otherwise, you could benefit from a travel rewards credit card. Offered by banks, credit unions, airlines, and hotel chains, these credit cards allow you to earn miles or points that can be redeemed for flights and hotel stays. Plus, you could be looking at no foreign transaction fees for international trips — it all depends on the card.

For cash back collectors: If your goal is to get the most bang for your buck on everyday spending, then a single cash back credit card is what you need. Seek out options that offer high cash back percentages on groceries, gas, or dining.

For the ones who want to build (or rebuild) their credit: If you’re starting from scratch, one to two low-limit or secured credit cards could be your best bet. While smart use of a credit card is one of the most common ways to improve your score, there are alternative methods to build credit.

If a rewards card is your top pick, make sure you know how to make the most of it.

In addition to goals, there are your interests. Do you want to see more of the world? There’s a card for that.

How to Determine if You Have Too Many Credit Cards

By now, you may have an idea of how many credit cards you’d like to keep. If you don’t, that’s okay. Here’s some additional information to guide your decision-making.

Risks and Rewards of Having Multiple Credit Cards

There will be warning signs if you have more credit cards than you can handle. And if you’ve settled on your ideal number, that will show too.

Let’s take a look.

The Impact of Multiple Credit Cards on Your Credit Score

We’ve briefly explored how keeping multiple cards can affect your financial standing, but let’s get into the details a bit more.

Having multiple credit cards can sometimes boost your credit score, and in turn, creditworthiness. A higher total credit limit, more lines of credit, and a lower credit utilization is what you want to aim for when adding a card to your collection. This combination signals to potential lenders that you’re a responsible borrower.

However, multiple credit cards can hurt your score too. Opening a new account or opening too many too quickly will ding your score due to hard inquiries. A single hard inquiry reduces your score by five points or less. Several inquiries will add up.

Your score will also drop if you don’t make full or regular payments on your cards.

The Importance of Credit Utilization Ratio

Your credit utilization ratio or rate is calculated by dividing your total outstanding credit card balances by your total available credit limit, then multiplying the result by 100 to get a percentage.

It’s a key metric for lenders — and for you. In fact, it makes up 30% of your FICO® score and 20% of your VantageScore® credit score.1 More credit cards can help keep your ratio low and under 30%, which is what experts generally recommend. A low ratio makes for a better credit score, as long as you’re practicing smart spending and paying balances when they’re due. Fun fact, people with the highest credit scores typically use less than 10% of their available credit.

Understanding the 2/3/4 Rule for Credit Cards

While not a strict industry standard, the 2/3/4 rule is a guideline some issuers use to prevent borrowers from opening too many credit card accounts in a short period, ultimately protecting your credit score.

Think of it like introducing new herbal supplements to your diet. When you start on your first supplement, you need to give your body some time to adjust and pinpoint any side effects. Only then can you fully commit to the next one. Similarly, spacing out your applications allows your credit score to bounce back after a hard pull.

Handling Credit Card Closures Without Hurting Your Credit Score

As you open new credit cards, you may slowly stop using your old ones. Unused cards aren’t a problem unless the issuer decides to close them for inactivity. The consequences of that? A reduction in available credit, the average age of your credit accounts, and your credit score. Since credit card companies are not required to notify you, it’s easy to miss this important update.

As a best practice, you should keep your credit card accounts open, even if that means maintaining very low balances. This preserves your credit score.

As a best practice, you should keep your credit card accounts open, even if that means maintaining very low balances.

Monitoring Your Credit Score

Your credit score is like the pulse of your financial health, and your credit report is the summary notes from a doctor’s visit. Planning to add more lines of credit? Then watch it closely.

Regular credit report checks allow you to:

- Catch errors early: Mistakes on your credit report can drag your score. Dispute inaccuracies right away.

- Track your progress: As you make positive financial decisions, like paying down debt, you’ll see your score improve. This can be a great motivator!

- Understand your borrowing power: Knowing where you stand can give you an idea of the kind of credit card interest rates or loan terms you’re likely to qualify for.

Tips for Effectively Managing Multiple Credit Cards

We’ve discussed timing credit card applications, maintaining low balances, auditing your spending habits, and the power of balance transfers, but there’s more. With a little organization and this list of savvy tips, you can master the art of rotating credit cards — whether you’ve got two or four.

- Automate minimum payments: Every credit card you open has its own terms and conditions including a unique interest rate, minimum payment amount, grace period, and due date. If keeping track of it all becomes a challenge, you can request to change all your due dates to the same day. Even better, automate your end-of-cycle payments. It’s the easiest way to avoid late fees.

- Set up account alerts: You may choose to receive them by text or email. Alerts allow you to quickly identify any suspicious charges and stay on top of all aspects of your accounts. Just be sure not to fall prey to promotional offers, which can lead to unnecessary spending.

- Review statements: Dedicate a specific time to review all your credit card statements and account summaries. This is how you get a holistic view. Make note of your total used credit and spending patterns. And make sure you’re not getting too close to the card limit.

- Compare interest rates: Look at the interest rates on your cards periodically. Prioritize paying down the one with the highest APR.

- Conduct a rewards assessment: On the anniversary of each card, evaluate whether the benefits you’ve received over the past year justify the annual fee. If not, consider downgrading to a no-fee version of that card from the same issuer.

- Implement a spending freeze: If you find yourself overspending, it’s time for a temporary “freeze” on one or more of your credit cards. This forces you to rely on other funds (maybe from your high-yield savings account) and reset your spending habits. Another option is to set a spending limit.

- Redeem rewards: Don’t let your hard-earned rewards languish! Schedule regular times to redeem your cash back or points.

- Designate digital wallet cards: If you use digital wallets, make it a point to label each card with its primary purpose. This helps you select the right card at the point of sale.

- Play around with credit score simulators: Use an online credit score simulator to see how different actions, such as opening a new card, might impact your score.

- Opt for two-factor authentication (2FA): It’s there to help you. With two-factor authentication enabled, you have an extra layer of security beyond your password. That’s one of the ways to keep unauthorized users out.

If you find yourself overspending, it’s time for a temporary “freeze” on one or more of your credit cards.

FAQ

Let’s clear up any last-minute queries.

For some, five or more credit cards might be manageable, but for others, this number could be overwhelming. If you have multiple cards and you find yourself spending on impulse, carrying high balances, or struggling to track and make payments, then it’s time to reassess your optimal number of cards.

Again, there’s no right or wrong answer. Treat this decision as if you were picking more than one checking account. If you’re newer to the world of credit, one or two cards is a good baseline.

There’s no set number, but generally, two to three well-managed credit cards can allow you to maintain a credit score of 750 or higher. Take note — you generally need a score of 670 to get a rewards credit card, and a score of at least 660 for a regular credit card.

It’s not necessary to get a store credit card just to build credit. Responsible use of a major credit card gets the job done. But if you shop frequently at a particular retailer and can manage monthly payments, then there’s no harm in signing up for a store credit card. Plus, you could benefit from special discounts.

That depends on your lifestyle and interests, as well as your future plans. Do you want to take advantage of statement credits on one card and a double-the-points deal on another? If both cash back and airline miles matter to you, then multiple rewards cards it is! Use our roundup of tips to make card management simple.

Think of it this way — a few well-managed high-limit credit cards can offer more breathing room when it comes to your credit utilization ratio. On the other hand, several low-limit credit cards require careful tracking to avoid maxing out. It boils down to what you can comfortably manage without overspending.

The types of credit cards you carry should align with your financial lifestyle and goals, which in turn, influences the number of cards you need. For instance, a frequent flyer might benefit from a travel rewards card and a general-use card, while someone pursuing debt freedom might go from three cards to one in an effort to consolidate their balances with a balance transfer.

The Takeaway

Evaluating your credit card usage is an important part of financial wellness. If you’re happy with your current number of cards, shift your focus to working on other areas of your finances.

But if you’ve decided to add another credit card to your wallet, then it’s time to start researching. The good news is there are lots of great options out there to help you build your credit, maximize rewards, and reach your top financial goals.

Footnote

- FICO® is the registered trademark of Fair Isaac Corporation. VantageScore® is the registered trademark of VantageScore Solutions, LLC.

Credit Cards for the Way You Live

See the card options and rewards you could earn with PenFed.