CHECKING & SAVINGS

Top Tips for Transferring Your Money

What you'll learn: To make fast and secure money transfers, whenever you need to.

EXPECTED READ TIME: 7 MINUTES

You know that frantic sprint through a busy airport — the clock ticking, security lines at a standstill, and your gate feeling a mile away? Transferring money can feel a little bit like that, especially when you’re stuck in a teller line or navigating an unfamiliar funds transfer portal.

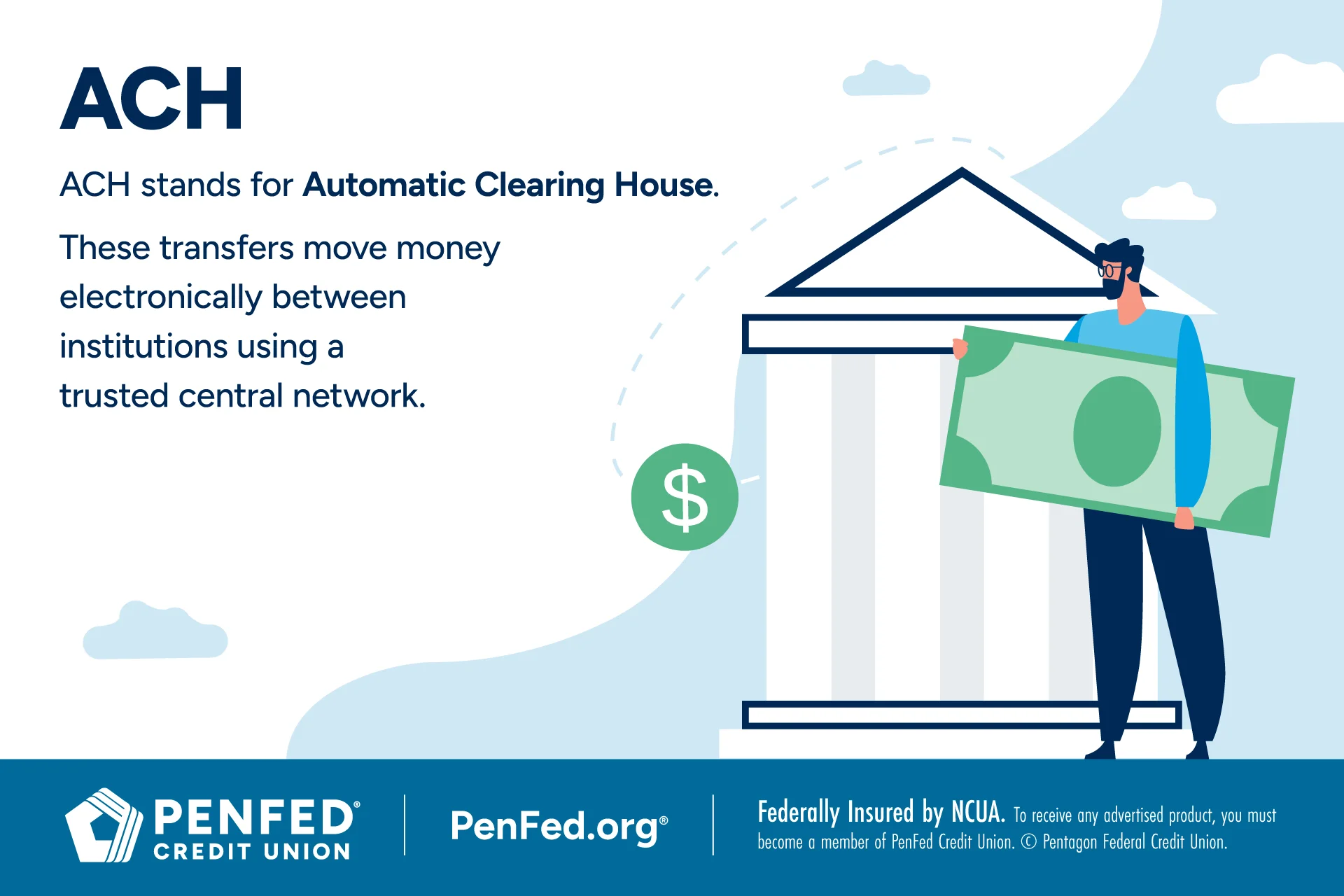

So, what’s your call when you need to move your hard-earned money securely and fast? Should you go for the widely used ACH (Automatic Clearing House) transfer or rely on the latest personal finance app?

Let’s take a look at what’s available to you and chart your course for seamless, stress-free money movement.

What Is a Money Transfer?

A money transfer is simply the movement of funds from one person or entity to another. Historically, this meant physically moving cash or using checks. Now, the process is fully digitized, with less risk of loss or theft and way more convenience.

How Do Money Transfers Work?

Good question! There’s a whole fleet of options to choose from when it comes to moving your money. The mechanics, speed, and cost will depend on the vehicle you pick.

Let’s explore some common types of transfers.

Bank-to-Bank Transfers

When you initiate a transfer, you’re giving your dollars their marching orders. Here’s the inside scoop on how your money gets from point A to point B:

- The journey begins in your banking app. Log in, select the “transfer” function, then decide how much you want to send.

- Now, it’s your bank’s turn. After receiving your request, they’ll send out a digital instruction through a secure network.

- Here’s where the magic happens. The instruction arrives at a central clearing house, where it’s digitally verified and directed to its destination.

- In this step, the recipient’s bank receives that same digital instruction, and after a final check, it credits the account.

This intricate and secure process is what we call an ACH transfer. It typically takes a few business days. Several financial institutions batch requests together, which adds a bit of time but makes the process efficient and low cost (for both bank and customer).

Whether you’re transferring funds between checking accounts or from your everyday account to a savings fund, an ACH transfer is a viable method.

Wire Transfers

An emergency hits, and a loved one needs some cash right away. What do you do?

A wire transfer could help. This type of transfer is like a high-speed jet, ensuring your funds land right where they need to within hours. However, the speed comes at a cost, with fees ranging from $15 to $50.

That phone in your hand is part communication tool, part financial command center.

Old-School Money Transfer Services

Before digitized banking, there was Western Union and MoneyGram — the titans of money transfers. Thanks to these services, even individuals without bank accounts could send money, and you can still walk into one of these service locations to transfer cash. It’s a great option if you or the recipient need paper money pronto, or if the recipient lives overseas.

And while many brick-and-mortar locations are still standing, these services have also adapted with the times to allow you to complete money transfers with a few taps on your phone (if you do have a bank account). Just link your bank account in their apps.

Digital Wallets and Payment Apps

That phone in your hand is part communication tool, part financial command center. It’s home to digital wallets like Apple Pay and Google Pay, as well as peer-to-peer (P2P) payment services like Venmo, Zelle, and PayPal. Each offers a range of services from bill pay to splitting the cost of a meal or weekend trip with friends.

ATM Transfers

You can transfer funds between your accounts at the same bank or credit union using an ATM. This is a great option if you’re already at the ATM for another transaction.

Other: Brokerage to Bank

Maybe you recently sold some of your investments or need a portion of the funds in your portfolio for a big purchase. You can transfer money from your brokerage account to your linked bank account. It usually takes a few business days.

Other: Retail Partner Deposits

Some banks and credit unions now let you use your app to find a retail partner (like a local grocery or drug store) that accepts cash deposits. All you have to do is bring your money to the location and hand it over at the register. In minutes, it’s available in your account and ready to transfer or use for bill payments.

Some banks and credit unions now let you use your app to find a retail partner (like a local grocery or drug store) that accepts cash deposits.

How to Make a Transfer

Moving your money is generally straightforward, but the steps may vary by bank or the service you’re using, as well as the type of transfer.

Wondering about the step-by-step for common transfers? Here’s what it might look like:

External Transfers (Bank to Bank)

- Log into your online banking portal or mobile app.

- Navigate to the “transfer” or “payments” section.

- Choose between an internal and external transfer.

- Select the account you’re sending the money from and the account it’s going to. You may need to add the recipient’s bank details (bank name, routing number, and account number) if you haven’t already.

- Enter the amount you wish to transfer.

- Review all the details carefully, then submit the transfer. Keep your confirmation handy.

Mobile Apps

Most financial institutions have apps that mirror the functionality of their online banking sites. In fact, many of them allow you to send money using just an email address or phone number. This feature is usually powered by Zelle. This makes transferring money on-the-go super easy. Plus, features like biometric login add an extra layer of convenience and security.

How Long Does It Take to Transfer Money?

Wondering why some transfers fly and others stroll? Let’s find out.

Instant (within minutes or seconds)

P2P services like Zelle lead the pack, often delivering funds in seconds. Moving money between your accounts at the same institution is also instant. This lightning-fast speed is possible because the transaction usually stays within a single, integrated network. These types of transfers are generally free.

Same Day (within hours)

Wire transfers are the quintessential example. These transfers often cut out the intermediary (AKA the clearing house) to get those funds moving fast.

1-3 Business Days

This is the pace for most ACH transfers, including direct deposits, the majority of bill payments, and transfers between different banks. ACH transfers are almost always free.

3-5 Business Days

This longer timeline applies to less common transfer methods or those requiring extra security checks, especially for large sums or international transfers. For example, cashing out certain investments from a brokerage account might take a few extra days for processing.

Here’s a tip — some credit unions may facilitate money transfers quicker than big banks. Think early direct deposit. How and why? Well, because they’re member-owned and focused, these institutions may have more flexibility in their operational policies. That’s not to say that security lags — it remains a priority with advanced, foolproof technologies. Plus, credit unions must adhere to the National Credit Union Administration (NCUA) standards.

Check with your credit union to learn the specifics of money transfers.

4 Tips for Timing Your Account Transfers

Now that you know how long different money transfers take, let’s explore some tips and tricks for a seamless process.

1. Check the Calendar: Business Days vs. Weekends

The key phrase here is “business day.” Saturdays, Sundays, and federal holidays are like rest stops where your money pauses until the next working day.

2. Check the Clock: The Daily Cut-Off

Timing is everything — even on business days. Banks and credit unions have a cut-off time for processing transfers. If you hit “send” after that time (ranges from late morning to afternoon), your transfer won’t be processed until the following business day.

3. Check the Status

Hitting “send” is just the start. Let’s say you’re paying a security deposit on a new apartment. The landlord wants the funds by the first of the month. You initiate an ACH transfer on the 31st, the day before, believing you’re all set. But that in-app confirmation was only to tell you your transfer request has been received.

You can usually see the status of your transfer in your transaction history. The all-clear signal is when the “processing” status is no longer there, and the funds are out of your account. Other key terms to help you keep track of your money are:

- Sent: You may see this right after you initiate the transfer. Remember, it doesn’t mean “received.”

- Delivered/Available: This is when the funds have arrived in the recipient’s account and are ready for use.

When in doubt, time your transfer to arrive earlier than it needs to.

4. Check the Destination

International transfers are an entirely different ballgame. Factors like time differences, holidays in the recipient’s country, and currency conversion could lead to longer processing times.

When in doubt, time your transfer to arrive earlier than it needs to.

The best way to save money is to set recurring transfers and forget them.

How to Automate Transfers to Save Time

Imagine a world where your bills are paid, your debt shrinks, your savings grow, and you have the freedom to do what you want with your funds. That’s the magic of automating money transfers. Here are four ways to make it happen.

1. Grow your savings and investments

The best way to save money is to set recurring transfers and forget them. Think of it like this — each payday, an invisible hand moves money into your emergency fund, retirement account, or vacation fund. You decide how much. What’s left for you to do? Sit back, relax, and cash in when the time comes around.

Bonus tip 1: Take advantage of compounding with consistent contributions to your high-yield savings or investment account. The money you save earns interest, and then that interest starts earning its own interest. It’s a big win!

Bonus tip 2: If your bank or app offers the “round up the change” feature, then turn it on! It’s a great, low-effort savings hack. Every time you make a purchase, the transaction is automatically rounded up to the nearest dollar. That spare change is then transferred to your savings account.

2. Pay your bills and avoid late fees

Automate bill payments and kick stress to the curb. Most banks, lenders, utility companies, and service providers (phone, internet, medical services, etc.) offer options to set up recurring payments right from your account. This means you’ll never miss a due date and protect your credit score in the process (where applicable). If you choose to use this option, make sure to first read the terms and conditions, including how to terminate the automation and how long it takes the termination to kick in.

3. Double down on debt repayment

If you’re on a mission to become debt-free, automating payments can make all the difference. When you set up an automatic transfer that’s slightly more than your minimum payment, you start to make a nice little dent in that balance — and you don’t even have to think about it. Even an extra $20-$50 paid on a regular basis can save you hundreds in interest over the life of a loan.

4. Support loved ones, easily

Whether it’s an allowance for your child, helping an elderly parent, or making regular donations to a charity you care about, auto transfers are a game changer. The money arrives like clockwork, giving the recipient peace of mind plus you don’t have to go through the hassle of remembering to send it each month.

The Takeaway

Remember the scene of that frantic airport sprint? Now, you have your boarding pass — a clear game plan to move your money without the chaos. You’ve learned that every transfer has its own journey, from the instant speed of Zelle to the steady pace of ACH transfers. You decide what works for you.

Take Control of Your Finances

Get the checking account that allows you to do more.