FINANCE

Your Savings Era: Retirement Strategies Based on Age Group

Expected read time: 6 minutes

You’re the only person who knows what you want your golden years to look like. That means you’re the only person who knows how much you’ll need to save. However, looking at suggested benchmarks for retirement based on age can help you decide if you’re on track or need to adjust your strategy.

Are Savings Benchmarks Useful?

Savings benchmarks are popular financial tools because they’re simple. But a benchmark doesn’t replace more careful financial planning.

Your retirement savings need to match your unique retirement goals. Want to retire early? Take time off work when you have kids? Then you’ll need to adjust your savings habits to match those choices.

You may also have to adapt to obstacles like job loss or major illness that temporarily derail your progress. A retirement calculator can give you a better estimate of what you’ll need, or you can work with a financial advisor to really customize your plan.

The important thing is not to let benchmarks discourage you. You may not be where your peers are, but that doesn’t mean there aren’t ways to catch up if you’re behind. Benchmarks are just starting points.

A retirement calculator can give you a better estimate of what you’ll need.

Saving in Your 20s

Many financial experts agree that you should save around 15% of your annual income for retirement (including your employer contribution) each year. That may seem impossible if you’re just starting out with an entry-level salary, renting your first apartment, paying for school — the list goes on. But saving in your 20s is important because of compound interest.

You should save around 15% of your annual income for retirement.

Don’t give up if you can’t afford to save the recommended amount right now. Consistency is the most important factor. Start with what you can afford and increase as possible, and check out our tips for helping you get started saving for retirement in your 20s.

Checklist for Success in Your 20s

Even if you’re unable to save as much as you’d like, there are concrete steps you can take to get your retirement off to a good start. They include:

- Set up a retirement account. If your employer doesn’t offer retirement benefits, don’t sweat it. You can create your own account.

- Create a budget. You’re much more likely to save if you actively manage your money.

- Open a great checking account. Free checking will help you keep more money by ditching fees, and interest-bearing accounts can even earn you a little extra.

- Manage your debt. Don’t let debt keep you from saving. Learn how to take control of student loans, auto loans, and credit cards so you can reach your goals.

Saving in Your 30s

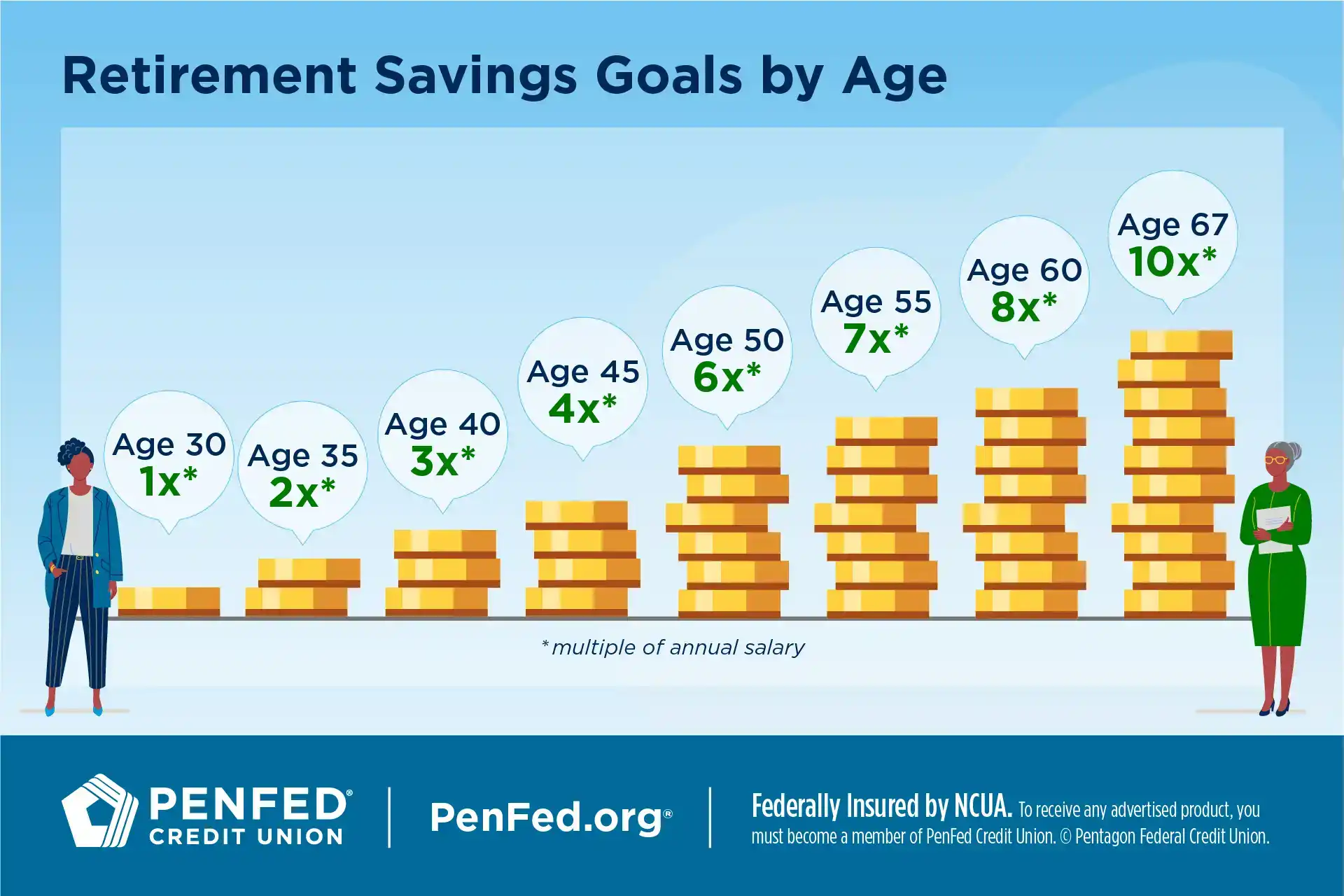

By age 30, you should have saved one year’s salary, with the goal of increasing that to two times your annual salary by 35.

Saving in your 20s and 30s is especially important because with time, compound interest will greatly increase your savings — and you have the most time when you’re young. However, it can be tough to prioritize retirement if you’re getting married, buying your first house, or having kids. You may also still be carrying student debt.

Saving in your 20s and 30s is especially important because with time, compound interest will greatly increase your savings.

A few things can help. If possible, get a job that offers an employer match and save enough to get the full match. Until then, be sure you’re maxing out contributions to Health Savings Accounts (HSAs) and Individual Retirement Accounts (IRAs) or similar retirement products. Retirement accounts and HSAs are important because they’re taxed differently, allowing you to keep more of your money.

You can also set up savings tools like high-yield savings accounts and certificates to earn additional compound interest if you’ve maxed your HSA and IRA. These accounts offer guaranteed returns at predictable rates regardless of market factors.

Get a job that offers an employer match and save enough to get the full match.

Checklist for Success in Your 30s

Use your 30s to strengthen the foundation you laid in your 20s and you’ll see your retirement savings start growing faster. Try:

- Setting up a retirement account (if you haven’t already).

- Funding savings tools that offer guaranteed yields with little or no cost.

- Automating your retirement contributions and savings. You’re more likely to save money if it doesn’t hang around in your checking account.

You’re more likely to save money if it doesn’t hang around in your checking account.

Saving in Your 40s and 50s

By age 40, you should have saved three times your annual salary with the goal of increasing that to four times by 45 and six times by age 50.

If you’re still carrying bad debt, now’s the time to kick it to the curb. It’s also not a bad time to pick up a side hustle or establish passive income streams. Use your skills from work to land freelance jobs, or monetize your crafts or hobbies. You can use those savings tools from your 30s to cover startup costs or invest in higher-yield products, or fund them more heavily if they’re performing well.

If you’re still carrying bad debt, now’s the time to kick it to the curb.

You may need to make some hard choices and prioritize yourself at this stage. That could mean steering your kids toward scholarships instead of paying the full cost of school or waiting a little longer to splurge on your dream car. You don’t have to quit living life — you just have to live with an eye on future good times.

Checklist for Success in Your 40s and 50s

Make the most of middle age by:

- Paying off bad debt (if you haven’t already).

- Establishing side hustles and passive income streams to generate more savings.

- Reinvesting or building your savings from your 30s.

- Increasing your retirement contributions and reinvesting retirement funds from old accounts.

- Prioritizing yourself and keeping an eye on the future.

Saving in Your 60s

By age 60, you should have saved eight times your annual salary with the goal of increasing that to 10 times your annual salary by age 67, the average age of retirement in the U.S.

You’re in the home stretch! Now is the time to take stock of your remaining assets, liabilities, and benefits. Gather up your documentation, start filling out forms, and make sure you understand your Social Security and Medicare benefits.

Pay off any substantial remaining debts, like your mortgage or auto loan, and revise your personal budget.

If possible, pay off any substantial remaining debts, like your mortgage or auto loan, and revise your personal budget according to your new lifestyle and income. You may also want to consider going part-time for a while before fully retiring so you can stash a little more cash.

Delay drawing your retirement until you absolutely need it. The longer you leave it, the more time it has to grow. Evaluate your assets and consider whether you need to adjust your mix to better protect and grow your savings. Don’t forget that you’ll be taxed on withdrawals from some types of retirement accounts like 401(k)s and traditional IRAs.

Checklist for Success in Your 60s

Even in your 60s, there are ways you can work toward a better retirement. You can:

- Determine your assets, liabilities, and benefits, and gather necessary documentation.

- Pay off substantial debts like your mortgage or car loan.

- Delay drawing your retirement and let it continue to grow.

- Adjust your mix for a balance between growth and security.

- Plan for taxes on withdrawals from your retirement accounts.

Saving in Your 70s

Not ready to stop working? You don’t have to!

The 2020 Further Consolidated Appropriations Act removed an age limit that kept people 70 years and older from contributing to IRAs. That means you can continue earning — and saving — as long as you’re willing and able to.

The Takeaway

No matter how late you’re starting, there are effective ways that you can save for the retirement of your dreams. It’s never too late, and today is the best day to start.

Find Your IRA

It’s never too early to think about your future.