FINANCE

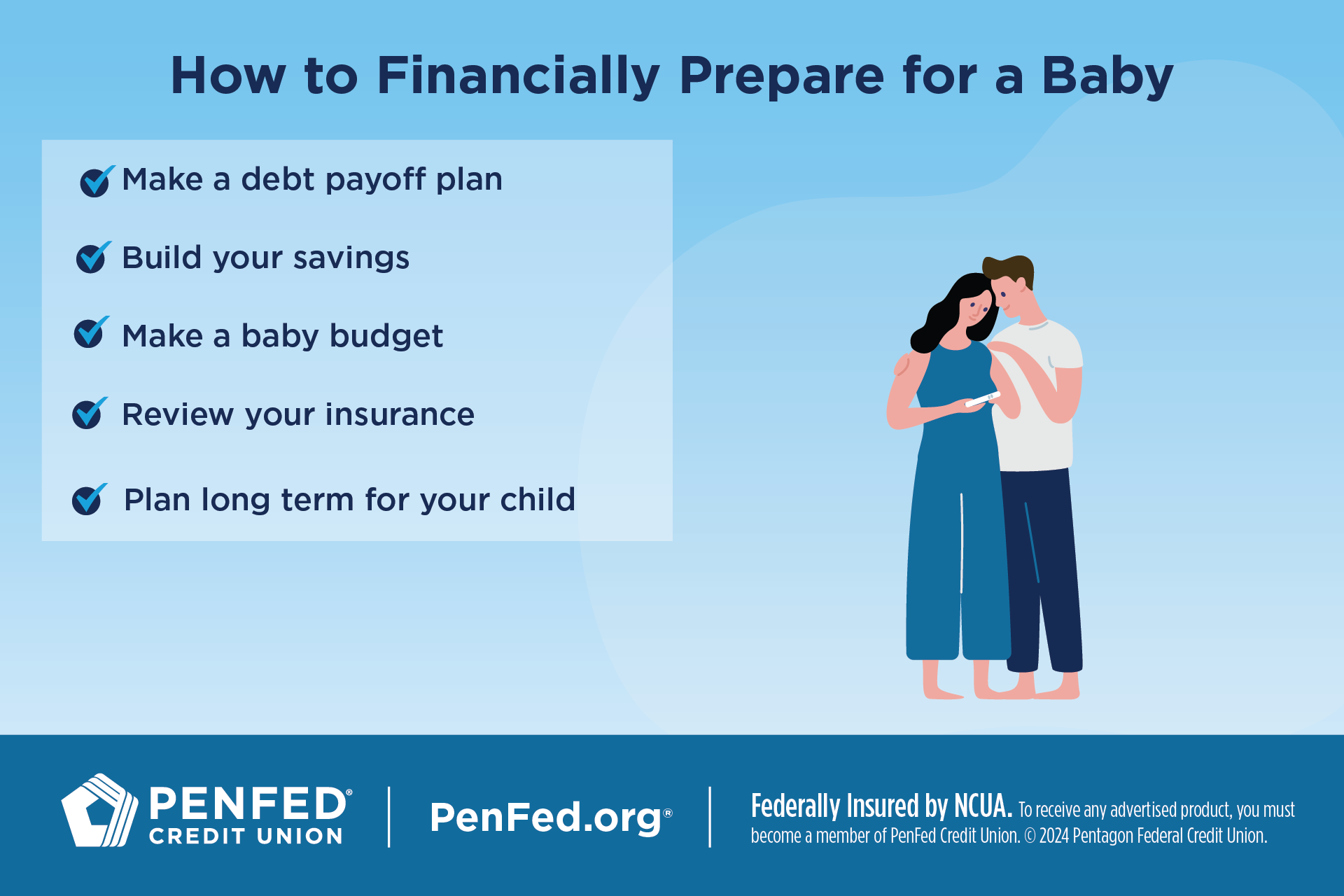

How to Financially Prepare for a Baby

EXPECTED READ TIME: 6 MINUTES

"Prepare for arrival" takes on a whole new meaning when there’s a baby on the way. Planning for a baby financially can ease the transition to parenthood and help you more fully enjoy the priceless experience of raising your child.

Check out these best practices for financial planning when you have a little one on the way.

Make a Debt Payoff Plan

Paying off debt will make it easier to take on the costs of a new baby. Although you might not be debt-free by baby's arrival, could you pay off your car loan or another small debt?

Choose a payoff strategy you can stick to. If you have high-interest debt from a personal loan or credit cards, debt consolidation could reduce your interest charges and help you pay off your debt faster.

Cut Unnecessary Spending

Survival mode is a common trigger for overspending, especially when you haven’t slept in days and you’re trying to figure out if your baby’s crying is due to colic or teething or a sudden temperature dropped from 73 to 72 degrees in the nursery.

It’s going to be way easier to stick to a postpartum spending plan if you make room in your budget now for unpredictable costs.

Try to avoid unnecessary purchases, especially if they require piling on more debt. Look at your monthly expenses to get an idea of which costs you might be able to eliminate or scale back. You can even download an app that tracks your money to help you budget consistently and identify waste.

It’s going to be way easier to stick to a postpartum spending plan if you make room in your budget now.

Build Your Savings

Building up your savings before you take parental leave will help you better meet your new financial responsibilities. Automating your savings can help.

If you have the means, opening a high-yield savings account and contributing to it monthly could help you grow your savings more quickly thanks to its higher APY (annual percentage yield). Some high-yield savings accounts have monthly maintenance fees and minimum balance requirements, so shop around.

Emergency Fund

Now is the time to start or grow your emergency fund. Best kept separately from your other savings accounts, your emergency fund is what you can turn to for literal emergencies such as the loss of a job or unexpected medical or home-repair bills. As a rule of thumb, aim to save at least three to six months' worth of living expenses.

As a rule of thumb, aim to save at least three to six months' worth of living expenses.

Save For Parental Leave

Do you know if your employer offers paid parental leave? Not all of them do, so make sure to brush up on your employer's policy so you can plan accordingly.

The Family and Medical Leave Act (FMLA) provides eligible employees with up to 12 weeks of unpaid, job-protected leave each year. Eligibility is up to your employer, however, and you may need to meet certain requirements such as having been employed for 12 months prior to the leave date.

If you’re not eligible for FMLA, you may be eligible for a shorter term of medical leave. Be sure to check with HR as soon as you’re ready to tell them you’re expecting.

Be sure to check with HR as soon as you’re ready to tell them you’re expecting.

If your employer offers paid leave, but not for your full salary, consider budgeting for the cut by putting a percentage of your paycheck into savings for at least three months prior to your leave. That cushion could help keep you from racking up debt on your credit cards during your leave.

If you'll be going from two incomes to one after baby's arrival, you may want to save for at least six months' worth of expenses before you give your notice.

Map Out Your Baby Budget

The good news that you're expecting may trigger the urge to buy everything baby. Before you start spending, make a plan to cover needs before considering wants. Budget for things like:

Diapers, wipes, clothing

Feeding items (bottles, breast pumps/formula)

Baby/personal care

Bath necessities/toys

Crib and bedding

Stroller and car seat

You can use a baby-costs calculator to create a budget. You can also shop around or ask friends and family for used baby gear to keep costs low.

If you plan on nursing, know that breast pumps can be expensive, but insurance will cover a portion or the entire cost of a breast pump. Ask your doctor or midwife about how to get one without paying full price. They should have ample resources to help you out.

You can also shop around or ask friends and family for used baby gear to keep costs low.

Be Practical About Your Registry

Creating your baby registry is definitely an opportunity to ask for wish-list items, but including practical items, such as diapers, bibs, and pacifiers, can help you save on everyday essentials.

Don't Forget Childcare

Childcare is a major cost for Americans, and demand is highest for ages 0-3. The current average pay for a babysitter in the United States is $21.73 per hour, while the average weekly cost of daycare is $314. While family and friends are often happy to help when they can, it’s likely there will still be times when you’ll need to pay for quality childcare. Even more so if you plan to go back to work.

Our advice: If you know daycare is in your future, start touring places as soon as you start trying for a child or as soon as you find out you’re expecting. Then budget a couple hundred dollars for enrollment fees to get on multiple waiting lists because your wait could be up to two years.

Budget a few hundred dollars for enrollment fees to get on multiple waiting lists.

Government Assistance for Childcare

If the idea of spending $1,500 a month on childcare sounds scary, there are programs out there to help. Even if you think you make too much money to qualify for assistance, it’s a good idea to check out what’s available in your state. You may be surprised to find out that you qualify.

Review Your Health Insurance

The cost of having a baby can vary widely depending on whether you have insurance and what your insurance covers. Review your insurance benefits so you understand what copays, deductibles, and other costs you will be responsible for.

Know this: Even if you already have insurance (or you aren’t covered at all), find out if you’re eligible for Medicaid while pregnant. Depending on your providers, Medicaid could significantly reduce your pregnancy and childbirth costs.

Even if you already have insurance, find out if you’re eligible for Medicaid while pregnant.

Looking ahead, set aside time to make sure your insurance will meet your family's changing needs. You may want to review or consider adding policies for:

Medical

Dental

Life

Disability

Most individual parent policies cover newborns for about a month after birth. In that time, you’ll enroll them under their own plan. And if you’re on Medicaid, your child should also qualify for Medicaid as well. Check with your local department of social services to be sure.

Most individual parent policies cover newborns for about a month after birth.

Plan for the Long Term

Your kids' expenses will be a long-time priority — the earlier you can get a jumpstart on saving for their future, the better.

Get Ready for School

Sending your little one off to college may seem like a lifetime away, but starting an education fund for your child early on is a smart step. Consider investing in a 529 plan for your child. A 529 plan is a tax-advantaged account that can be used for education expenses.

Another option is an education certificate. Money that’s locked into a certificate won’t be accidentally spent, earns a high APY, and offers a guaranteed return on investment.

Set Up Early Financial Success

Another great way to give your child a leg up is to start a savings account for them. Thanks to compound interest, even saving a small amount monthly will grow substantially by the time they finish high school or college. This money could eventually be a down payment on a car, house, or other important investment.

Consider Life Insurance

his would also be a convenient time to add your child as a beneficiary to your life insurance policy. If you don’t have a policy, consider buying one for you and your partner (if applicable) so your little one will be provided for no matter what.

You may want to purchase a policy for your child as well. While you might not think it’s necessary, buying a policy now could benefit your baby later in life.

You can write your own will or seek guidance from an attorney or planning services.

Write Your Will

Writing a will may seem daunting, but it’s essential since it outlines how your assets will be distributed and who will be your child's legal guardian if you die before they reach adulthood.

Depending on your preference and finances, you can write your own will or seek guidance from an attorney or planning services. Trustworthy online software can also help you consider legalities as you plan your estate.

Don’t Stop Saving for Yourself

Having a baby dramatically changes your priorities. You’re now thinking about your child’s needs much more than your own.

But having a baby doesn’t mean you should stop planning for your own financial future. It’s important that you continue saving for retirement even if those golden years seem far off. Retirement accounts only pay off if your money has time to grow, so don’t put off saving!

Having a baby doesn’t mean you should stop planning for your own financial future.

The Takeaway

Financially preparing for your baby is truly a win-win — you'll feel more secure in your own finances, and your child will be set up for success from day one. Whether you have eight months to go or three, taking even just a few of these steps will have you on the right track so you can spend even more time with your new bundle of joy.

Start Building Your Future

Compare top savings accounts to find the best option for you.