FINANCE

How Do I Improve My Credit Score?

What you'll learn: Everyday tips to improve your credit score.

EXPECTED READ TIME: 7 MINUTES

Unless you have the perfect credit score — which is rare — it’s always a good time to think about giving it some TLC.

You can improve your credit score by consistently:

- Paying bills on time.

- Keeping credit utilization below 30%.

- Paying down high-interest balances.

- Fixing credit report errors.

- Avoiding unnecessary applications.

- Using strategies like the 15/3 payment rule.

We’ll dive into the above strategies and more so you can get to a strong score and achieve big-ticket goals.

Understanding Credit Scores

Your credit score is a three-digit summary of how you’ve handled the debt to your name — it’s that simple. The two most common credit scoring systems, FICO® and VantageScore®, range from 300 to 850.

When your score is high, you get to skip the line and head straight to the front of the financial pack. You can walk into a dealership and negotiate the best interest rates on an auto loan, saving thousands on a car. And you can get approved for a mortgage with a manageable monthly payment or land that new apartment you love.

When your score is low, so is your negotiating power. You may get hit with sky-high interest rates and even be denied on your credit applications. Then, there’s the constant feeling of playing catch up.

Fortunately, a low score isn’t permanent, and we’re here to help you map out a plan to bounce back.

Your credit score is a three-digit summary of how you’ve handled the debt to your name — it’s that simple.

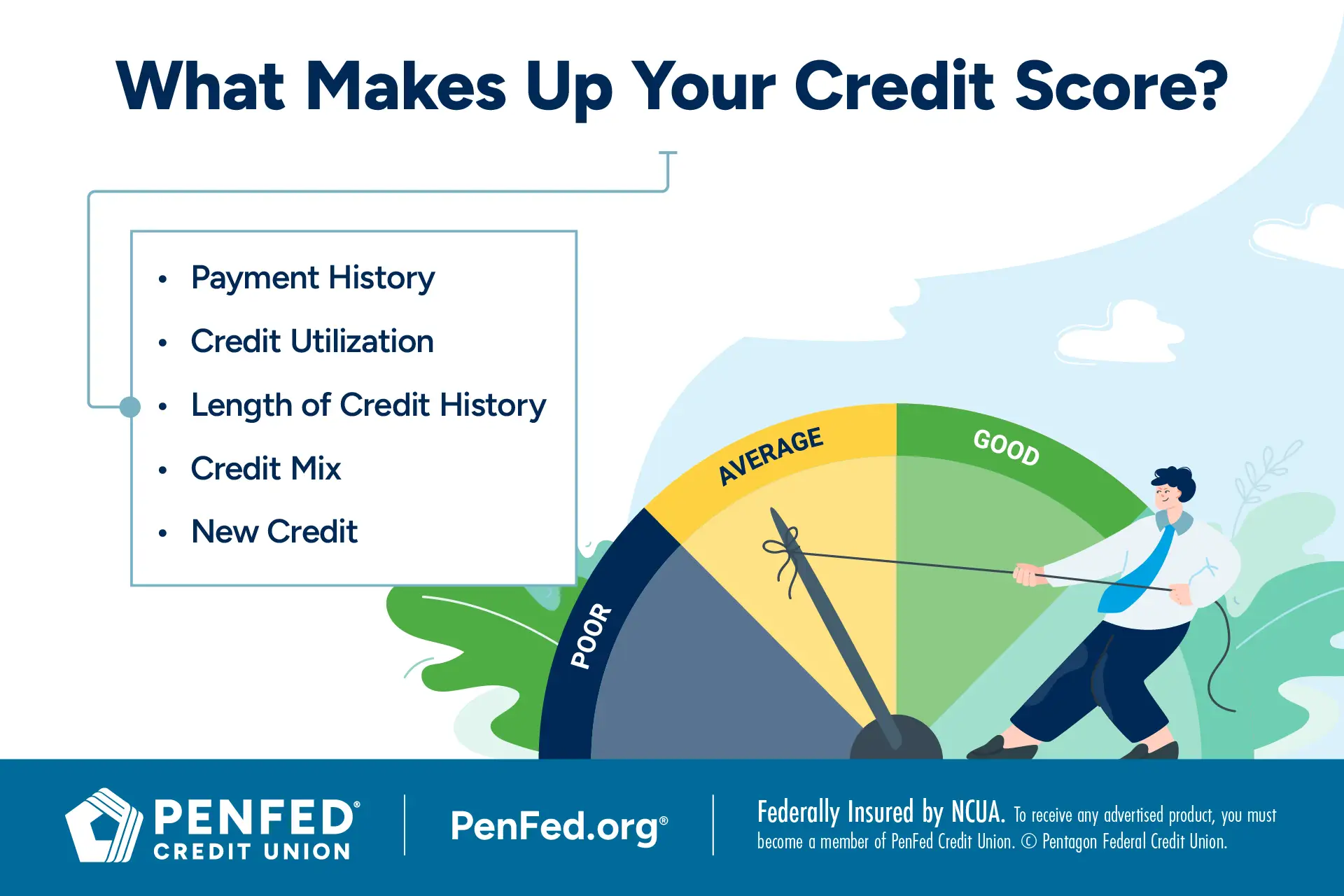

What’s In a Credit Score?

Knowing your score is one thing, but understanding how it's calculated is another. The exact makeup of your score might change slightly depending on the scoring system, but the core elements for building a powerful financial reputation are always the same.

Check them out in the visual below.

Actionable Strategies to Improve Your Credit Score

A few smart moves can make a big difference over time and get your score ready for the big stage. Let’s dig into five practical strategies for improving your score.

1. Pay Your Bills on Time

This one’s a no-brainer. When it comes to calculating your score, your payment history is the biggest piece of the pie.

Think of it like this — consistently making timely payments is like building muscle. Every on-time payment is a powerful rep, and the more you do, the stronger your financial core becomes. However, one late payment can undo months of hard work and stick you with unwanted weight in the form of late fees.

To make things simple, set up automatic payments for your credit cards and loans. That way, you'll never have to worry about missing a due date. If a bill is due on the 15th, set the payment for the 13th to give yourself a buffer.

2. Strategize and Pay Down High Balances

Ever heard of credit utilization rate? A big part of improving your score is reducing the total amount you owe and keeping it at or below 30% of your overall credit limit. Exceed that number and lenders might see it as a red flag. You don’t want to be the borrower blacklisted for “over relying” on credit.

Instead of trying to tackle all your cards at once, target the one with the highest interest rate and pay it down aggressively. This is what experts call the debt avalanche method. Once that first card is down to $0, roll that momentum into the next one on your list! Every dollar you pay frees up more of your available credit and lowers your utilization rate.

Pro tip: Worried about overspending? Many credit card companies let you lock your card right from their mobile app, so you can curb impulse swiping and keep your account active. Take full advantage of this feature.

Instead of trying to tackle all your cards at once, target the one with the highest interest rate and pay it down aggressively.

3. Request a Higher Credit Limit

This is a simple and quick way to improve your credit utilization rate alongside regular minimum payments. Let’s say you have a credit card with a $2,000 limit and a $1,000 balance. Your utilization is 50%, which is quite high. Fill out an application or get on the phone with your lender to ask if they can up your limit to $4,000. Best case scenario: they say yes, your balance stays the same, and your utilization drops to 25%.

4. Avoid Unnecessary Credit Card Applications

It’s tempting to sign up for that glossy travel rewards card plastered on every other billboard or the store credit card promising a sign-up discount, but each application ends with a hard inquiry on your credit report. While a single check for a credit card won’t do much damage (you’ll lose five points or less), a bunch of them in a short period can make you look risky to credit card lenders and knock some points off your score.

Instead of applying for new credit, consider using the cards you already have. Remember, improving your score is a marathon and you don’t need new gear at every aid station.

Pro tip: The rules are a little different if you’re after an auto loan or mortgage. Shop around and take advantage of the 14-to-45-day period where multiple hard inquiries typically count as one.

5. Become an Authorized User

Starting out or rebuilding your score? Then this strategy is for you. Sit your friend or trusted family member with the excellent credit history down and ask them if they would be willing to partner with you. If they agree, they’ll add you as an authorized user on their credit card. Then, the magic happens. Their good payment habits and low utilization will show up on your credit report, helping you score points.

The golden rule: Check your credit report often.

How to Monitor and Fix Credit Report Issues

Now, onto step two of improving your credit.

The golden rule: Review your credit report often (here’s how). It’s the only way to know where you stand, and for you to sniff out errors, which are more common than you think.

Where to Get Your Report

So, where should you go looking? AnuualCreditReport.com is your one-stop shop. Here, you can request one free copy of your credit report from all three major credit bureaus (Equifax®, Experian®, and TransUnion®). Get them all at once or space them out throughout the year — it’s up to you.

You can also check your credit score for free, as often as you want, through your bank or credit union. Many of these institutions offer credit monitoring tools to keep you in the know and on top of your finances.

Identifying and Disputing Credit Report Errors

Don your detective hat when you get those free copies of your report. Look for things that don’t belong, such as:

- Incorrect personal information: A misspelled name, wrong address, or Social Security number that’s off.

- Unauthorized credit inquiries and accounts: First time seeing it? Unfamiliar accounts could be a sign of identity theft.

- Incorrect balances or limits: Make sure that an account you paid hasn’t been reported as delinquent or your balance isn’t way higher than it’s supposed to be.

If you spot any of these errors, dispute them with the credit bureau and/or creditor that reported the information. The Fair Credit Reporting Act (FCRA) requires them to investigate and correct any mistakes, and when it’s all fixed, you’ll start gaining points.

Freezing Your Credit

You can stop identity thieves in their tracks with a credit freeze. Unlike locking your credit card, freezing your credit completely restricts access to your report. This means no new accounts can be opened without your permission.

Take control with these three steps:

- Register for an online account with each of the three major credit bureaus.

- Initiate a freeze right from your account dashboard — it’s free.

- Unfreeze your report online whenever you’re ready to apply for new credit.

To really improve your score, commit to paying your balances strategically and aggressively.

The 15/3 Credit Card Payment Rule and Other Useful Guidelines

You’ve learned what it takes to find and correct errors on your report. Now, let's talk about some advanced-level plays to build your score faster.

The 15/3 rule is a gamechanger for your credit utilization rate. It’s all about strategically timing your payments. The 15/3 method is simple:

- Make two payments on your credit card each month.

- First, pay off a large portion of your balance (enough to get your utilization below 30%) at least 15 days before your statement closes.

- Then, make a second payment to clear the remaining balance three days before your due date.

Why does this simple trick work? Most card issuers report your balance to the credit bureaus on your statement closing date (learn to decode your credit card statement here). By paying off a big chunk early, you ensure they report a much lower balance, which can bump your score.

Beyond the 15/3 rule, consider these power moves to help you win:

- Keep zero balance accounts open: Think of the average age of your accounts as your stripes in the game. It shows lenders you’ve handled credit responsibly over an extended period. Closing an old account, even a paid-off one, shortens that history and may drop your score.

- Pay more than the minimum: The minimum payment keeps you out of trouble but won't necessarily get you out of debt. To really improve your score, commit to paying your balances strategically and aggressively, dodging high interest charges.

- Consider debt consolidation: Tired of juggling multiple card payments? Debt consolidation could help. When you roll your balances into a single loan or balance transfer credit card, you go from several due dates and interest rates to just one. This simplifies management, helping you stay on track and protect your payment history. Before taking this step, estimate your savings with a balance transfer calculator.

- Practice the 2-2-2 rule: New to credit? Add this rule to your starter pack. It suggests you open two revolving credit accounts, with limits no less than $2,000. Keep both open and in good standing for at least two years. With this simple formula, you can establish a rock-solid credit history that allows you to do more.

Settling Up: When Your Account Goes to Collections

An account goes into collections when a creditor gives up on trying to collect a debt and sends it over to a third-party collection agency.

Finding out you have an account in collections can be scary, but it's not a dead end. You just have to be proactive.

Get a call or spot one on your report? Here are your options:

- Verify the debt: Your first move is to confirm the debt is actually yours and that the amount is correct. Under the FCRA, you have the right to request validation of the debt from the collection agency. Do this in writing.

- Negotiate: Don't assume you have to pay the full amount. Some agencies are willing to settle for less, sometimes up to 50% of the original debt.

- The Pay-for-Delete Strategy: This is a crucial step. Before you pay a single cent, negotiate a "pay-for-delete" agreement. This means you’ll pay the agreed-upon amount in exchange for the agency removing the negative account from your credit report. Make sure you get this agreement in writing before you pay.

Face collections head on and watch your score climb in the months after.

To get into the 700s, focus on the two biggest factors — payment history and credit utilization.

Reaching Good, Great, and Exceptional Credit Scores

Let's talk about what it takes to get to the top tiers and stay there.

Moving from 500 to 700

A score in the 500s is considered “poor” or “fair.” Look at it like a basic membership that comes with limited access and extra costs for certain features and services. While you’ll likely be able to secure a line of credit, be prepared to pay high interest rates (and potentially, other fees).

Aim to land in the 700 range, which is considered "good" to "very good." This privileged status is your ticket to reasonable deals on credit cards and loans.

To make this jump, focus on the two biggest factors — payment history and credit utilization.

Achieving an 800 Credit Score

A score of 800 or higher is considered “excellent” or “exceptional.” Only 24% of Americans have a score this high. Getting here is like earning a first-class membership with all the bells and whistles. It takes time and discipline, and it means:

- An excellent payment history (zero late payments)

- A very low utilization rate (often less than 10%)

- A long history of managing different types of credit responsibly

Remember that negotiating power we talked about? An 800-level credit score will make it happen.

While you can’t go from 500 to 800 overnight, you may see changes in 30 to 90 days when you consistently work toward it.

Is a 900 Credit Score Possible?

The simple answer is no — that is for the main FICO® and VantageScore® scoring systems. Both peak at 850. There are, however, other score ranges. For example, FICO’s industry-specific models start with a score of 250 and stop at 900.

To put your best financial foot forward, it’s essential to have a basic understanding of popular industry-specific scores.

- FICO® Bankcard Score: This is the score a card issuer uses to evaluate your application for a new card or limit increase. It gives them an in-depth picture of your risk to default for that specific product.

- FICO® Auto Score: As the name suggests, this score is for auto lenders. It allows them to predict the likelihood of you paying back a car loan.

FICO® constantly updates these scoring frameworks to ensure the fairest and most accurate weighting. You’ll usually need to pay something to access these updated, specialized versions (via the credit bureaus) as they may not be on your credit report. Learn more about each one on the official FICO® website.

Your Timeline for Building Credit

The journey to an improved score varies from person to person, but here’s a general timeline to help you get situated and recap the most effective tools.

Months 1-5: Lay the Foundation

- This is your training period. Get a secured credit card, become an authorized user on a friend or family member’s credit card account, or consider debt consolidation.

- Make all payments on time and in full.

- Stay on top of your credit utilization. Remember, below 30% is best, plus you can always lock your card if you have to.

Month 6: Build Momentum, See Progress

- Keep at those healthy habits from the first 150 days. Throw in the 15/3 or 2-2-2 rule.

- You’ve hit your stride. Your positive payment history is now showing up on your report, which comes with a score boost. The number of points will vary.

- Check in with your lender. You might be able to get a credit limit increase or even graduate to an unsecured card.

12+ Months: Solidify Your Score

- Welcome to the big leagues. Your credit history is past the six-month mark, and your score may even rank as “good.”

- You don’t need to click “Apply” just yet (especially if you’re following the 2-2-2 rule), but if you haven’t already, start to think about diversifying your credit mix.

24+ Months: Level Up

- You’ve done it! With two or more years of responsible credit use, you’re well on your way to an “excellent” score.

- The journey isn’t over. Keep an eye on your report, paying attention to the average age of your accounts as well as potential errors.

FAQ

Ready to conquer your debt and transform your credit score? Here are the final few knowledge bits to get you on your way.

As fast as it takes. Creditors report your balances and payments each billing cycle which is around 28 to 31 days. While you can’t go from 500 to 800 overnight, you may see changes in 30 to 90 days when you consistently practice those five strategies discussed and look for and fix potential score-dragging errors on your report.

Wondering what’s the sweet spot? It’s the number that gets you favorable terms on your line of credit and allows you to check off your goals. Anywhere in the 700s is great. In fact, the average FICO® credit score in the US as of February 2025 is 717, and 701 for VantageScore®.

Curious to see how your credit score stacks up against those of your peers? We’ve got you — here are the average FICO® credit scores for different age groups, as of 2024.

- Ages 18-27: 681

- Ages 28-43: 691

- Ages 44-59: 709

- Ages 60-78: 746

- Ages 79+: 760

These numbers are a general guideline, not a finish line. What really matters is the progress you make.

The Takeaway

By now, you’ve probably taken a peek at your score and you’re either close to where you want to be or realize you have some serious work to do. The good news is today’s score isn’t your final destination. It’s just a snapshot of the moment, and you now have the knowledge and tools to change it!

Selected Sources:

Almost Half of Participants in Credit Checkup Study Find Errors on Credit Reports | Consumerreports.org

The Average Credit Score by Age, State, and Year | Businessinsider.com

Understand, Get, and Improve Your Credit Score | Usa.gov

What Are the Different Credit Score Ranges? | Experian.com

Sources last accessed September 2025

Keep Tabs on Your Score With PenFed Checking

From no-frills banking to free credit score monitoring, see how PenFed serves you.