FINANCE

How Do Tax Credits Work?

What you'll learn: Tax credits reduce the amount of taxes you have to pay, possibly saving you hundreds of dollars. Click to learn how they work.

EXPECTED READ TIME:6 Minutes

Bigger may be better in some cases, but that’s never true when it comes to your tax bill. That’s why it’s important to claim every tax credit and deduction you qualify for.

If you’re confused about the difference between a tax deduction and a tax credit, you’re not alone.

We always recommend consulting a licensed tax professional for the most up-to-date tax laws and regulations. In the meantime, here’s a quick breakdown to help you understand these terms and how they might impact you.

What’s the Difference Between a Tax Credit and a Tax Deduction?

Tax credits and tax deductions are similar — both can save you money when it comes to paying the Internal Revenue Service (IRS) or your state revenue agency — but they work in different ways.

Deductions are subtracted from your income, reducing how much of your income is subject to taxes. But a tax credit kicks in after you’ve computed your income tax, reducing the amount of taxes you owe, dollar-for-dollar.

Tax Credits Are More Valuable Than Deductions

In most cases, tax credits save you more than tax deductions. Deductions reduce the amount you owe because they reduce your taxable income by making it seem like you earned less, but tax credits reduce the amount of tax you’ll actually pay.

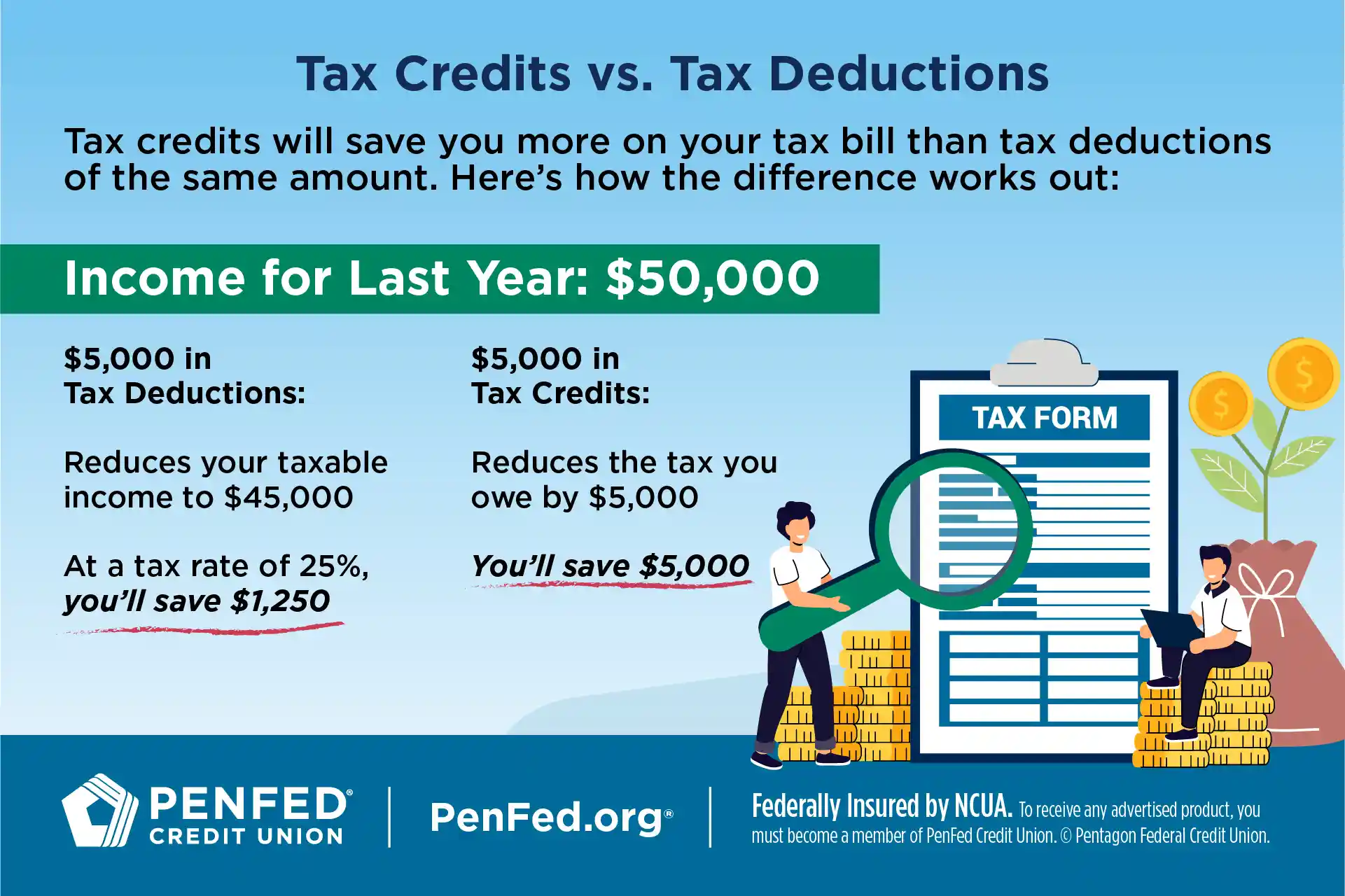

Here’s an example. Say you earned $50,000 last year. If you have $5,000 in deductions, then only $45,000 of your income will be taxed. You’ll be taxed at a rate of 25%, so by not paying that $5,000 you’ll save $1,250.

But what if that deduction was a tax credit instead? In that case, you’d save $5,000. That’s because a credit considers that amount of tax — the $5,000 — already paid.

In most cases, tax credits save you more than tax deductions.

Types of Tax Credits

There are three types of tax credits: refundable, nonrefundable, and partially refundable. All tax credits will reduce your tax burden, but they will be issued differently depending on the type of credit.

Nonrefundable

Nonrefundable tax credits are deducted from the taxes you owe. If your tax credits are greater than the amount of taxes you owe, the IRS will not issue you a refund for the difference. These tax credits expire once your taxes are filed and can’t be carried over to future years.

Common nonrefundable tax credits include the Lifetime Learning Credit and Child and Dependent Care Credit.

For instance, let’s say you owe $2,000 in taxes. You’ve already reduced your liability to $500. You diligently put money into your Individual Retirement Account (IRA) every month, and you're eligible for the Retirement Savings Contributions Credit (Saver's Credit) based on your age, filing status, and adjusted gross income (AGI). So you apply the maximum credit of $1,000. That eliminates the $500 dollars you owe but only uses half the credit. In this case, the IRS would not refund the remaining $500 and you could not claim that $500 next year.

Other common nonrefundable tax credits include the Lifetime Learning Credit and Child and Dependent Care Credit.

Refundable

Refundable tax credits allow you to claim a credit and refund on certain expenses. If your credit is greater than the amount you owe in taxes, the government will refund the difference to you through direct deposit or check.

Imagine you owe $2,000 in taxes. You’re working on a degree, so you claim the full American Opportunity Tax Credit of $2,500. That drops your tax liability to $0 with $500 of the credit left over. Because this is a refundable tax credit, the IRS will return that $500 to you as a refund.

Two popular refundable tax credits are the Premium Tax Credit and the Additional Child Tax Credit.

Two popular refundable tax credits are the Premium Tax Credit and the Additional Child Tax Credit. The Premium Tax Credit refunds taxpayers the cost of health insurance premiums purchased through the Health Insurance Marketplace. You may also be familiar with the Additional Child Tax Credit, which allows qualifying taxpayers to claim a child tax credit for an additional child.

Partially Refundable

Partially refundable tax credits are similar to refundable tax credits, except once your credit exceeds what you owe, the government will refund only part of the remaining credit.

Most partially refundable credits have a cap. For instance, The American Opportunity Tax Credit offers a credit of up to $2,500 for postsecondary educational expenses. If you’ve already reduced your tax liability to $0 before you’ve used the entire $2,500, then the IRS will refund up to 40% of the remaining credit. The refund cap varies from credit to credit.

Most partially refundable credits have a cap.

State Tax Credits

Tax credits are available on the federal and the state level in states that collect taxes. Many state tax credits are similar to those available on the federal level. For instance, many states offer an earned income credit just like the IRS does. But some tax credits may be specific to your state.

Can I Claim Tax Deductions If I Take the Standard Deduction?

When filing your taxes, you must choose between taking a standard deduction or itemizing your deductions. Since the standard deduction is now $14,600 per taxpayer, and even more for seniors over 65, itemizing won’t benefit most people unless they have a hefty home mortgage, a large amount of charitable donations, or huge medical expenses.

But even if you take the standard deduction, there still are a few more deductions you can claim and many credits for which you might qualify.

Itemizing won’t benefit most people unless they have a hefty home mortgage, a large amount of charitable donations, or huge medical expenses.

Popular Tax Credits and Tax Deductions You May Qualify For

There are hundreds of tax deductions you can qualify for, but some are more common. Here is a summary of some of the most popular deductions people claim:

Student Loan Interest Deduction: You may be able to deduct up to $2,500 of student loan interest if your income (for married couples filing jointly) is under $461,000 less than $95,000 on a single return (double that if filing jointly).

Educator Expenses Deduction: School teachers can deduct up to $300 for classroom supply expenses.

HSA Contributions Deduction: If you had high-deductible health coverage in 2024, you could contribute up to $4,150 to a Health Savings Account to pay for medical expenses ($8,300 for family coverage).

Retirement Plan Contributions: You may have a traditional 401(k) or other retirement accounts available to you at work. Contributions to plans such as a 401(k), 403(b), and profit-share plans are tax-deductible up to $23,000 ($30,500 if you are 50 or older). Contributions to traditional IRAs or other individual retirement accounts may also be deductible. You might also qualify for a Saver’s Credit of up to 50% of your first $2,000 in retirement plan contributions if your income (for married couples filing jointly) is under $461,000. The income limit for head of household filers is $34,500.

Education Tax Credits: If you’re paying for college for yourself or your kids, the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC) may help. The AOTC credit covers 100% of the first $2,000 you spend on education and 25% of the next $2,000. The LLC lets you claim 20% of the first $10,000 you paid toward tuition and fees. The income limit for claiming the AOTC or the LLC is $90,000.

Child Credits: You can get a Child Tax Credit of $2,000 per child if your income is under $200,000 ($400,000 on a joint return.) Also, you can get a Child and Dependent Care Credit of 20-35% of the first $3,000 for child and dependent care costs, or double that if there are two or more dependents. If you adopt a child, you can claim credit for up to $16,810 of adoption costs per child if your income is under $252,150. And if your income is under $59,899 as a single filer, you may also qualify for an Earned Income Tax Credit of up to $7,830, depending on your marital status and how many kids you have.

Residential Clean Energy Credit: You can claim a tax credit of up to 30% of costs if you install qualifying equipment in your home for solar, wind, geothermal, for fuel-cell energy. This is a nonrefundable credit, however, you can carry unused portions of this credit over to your next year’s tax return.

The Takeaway

From simple to complex taxes, TurboTax has you covered. And when you need help, real experts are standing by — and can even do your taxes for you, start to finish with TurboTax Live®. Getting your biggest possible tax refund has never been easier. And if you're a PenFed member, you can save up to $20 when you file with TurboTax. Click here to get started today!

The information in this article is for general educational purposes only and not intended to provide specific advice or recommendations. Please discuss your particular circumstances with an appropriate professional before taking action.

PenFed Has Teamed Up With TurboTax to Bring You Savings

Save up to $20 on federal products.