To apply for refinancing with PenFed, you will need:

- Your automobile’s VIN OR state of registration and plate number

- The name of your current lender

- Your personal identification information and documents

Rates starting at % APR*

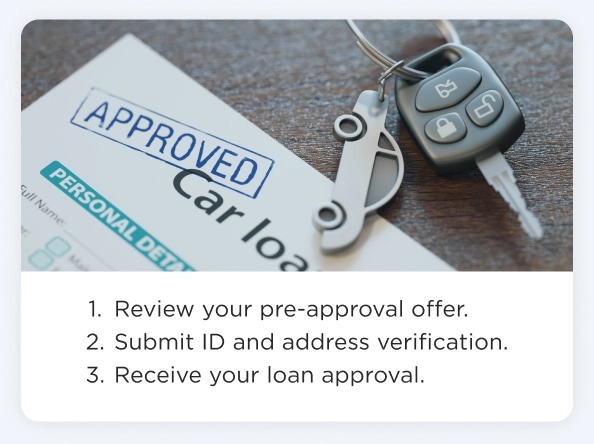

Pre-qualify with no impact to your credit score1

Won’t affect your credit score1

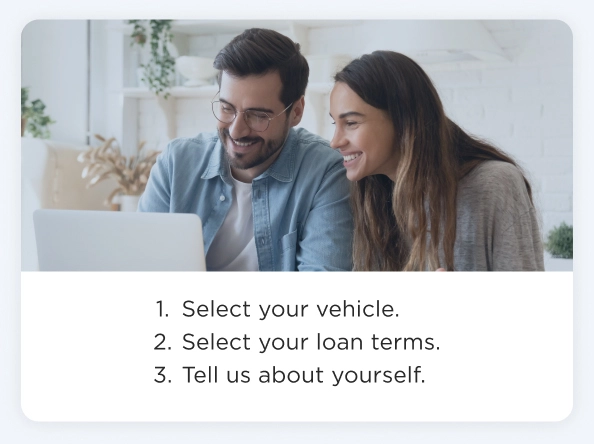

Apply Online

Get Approved

Finalize Loan

Won’t affect your credit score1

Estimated Monthly Payment for at APR*

| Current Monthly Payment | |

|---|---|

| PenFed Monthly Payment | − |

| Total Monthly Savings |

NEW

USED

|

36

Months

|

48

Months

|

60

Months

|

72

Months

|

84

Months

|

||||

|---|---|---|---|---|---|---|---|---|

|

New Auto RefinanceModel Year |

|

|

|

|

|

||

|

Used Auto RefinancePre-owned vehicles with 7,501 or more miles |

|

|

|

|

|

||

Model Year or newer & less than 7,501 miles

|

36 Months

|

|

|---|---|

|

48 Months

|

|

|

60 Months

|

|

|

72 Months

|

|

|

84 Months

|

|

Pre-owned vehicles with 7,501 or more miles

|

36 Months

|

|

|---|---|

|

48 Months

|

|

|

60 Months

|

|

|

72 Months

|

|

|

84 Months

|

|

*APR as low as

Your actual APR will be determined at the time of disbursement and will be based on your application and credit information. Rates quoted assume excellent borrower credit history. Not all applicants will qualify for the lowest rate.

To receive any advertised product, you must become a member of PenFed Credit Union which includes opening a $5 PenFed savings account.

Rates and offers current as of and are subject to change.

1The initial inquiry will be a soft pull that will not affect your credit score. If you choose to initiate a loan application after checking your rates, you will be required to authorize a full credit report inquiry, which would be considered a hard pull and may affect your credit.

*APR = Annual Percentage Rate. Your actual APR will be determined at the time of disbursement and will be based on your application and credit information. Rates quoted assume excellent borrower credit history. Not all applicants will qualify for the lowest rate.

††Average monthly payment savings of $191 per month was calculated based on the average monthly payments offered to PenFed members compared to their prior average monthly payments between Jan 1, 2023 and Mar 23, 2023. Each applicant's savings may depend on each applicant's new interest rate, term, and/or third party fees. For example, an applicant has a current vehicle loan with an amount of $24,227, an interest rate of 4.62%, loan term of 60 months, and monthly payment of $453. If that applicant refinances with PenFed for an amount of $24,227 an interest rate of % and loan term of 72 months, that member would have a monthly payment of approximately $399, and their average monthly payment savings would be $54. Your savings may be different.

Refinance Auto Loans: New vehicles are where you are the original owner and the vehicle is a current model year or newer and has less than 7501 miles. For used vehicles, maximum used car loan advance will be determined by PenFed using a JD Power value. Up to 125% financing is available in the U.S., Puerto Rico and Virgin Islands. PenFed does not permit internal refinances of an existing PenFed auto loan. For the 84-month loan term, eligible used vehicles must have model years as new as or newer than the current calendar year minus five years and less than 60,000 miles.

Rate depends on term. Vehicle weight and mileage restrictions apply.

Loan Payment Example: A $20,000 new auto loan financed at % APR would amount to 60 monthly payments of approximately $

each.