STUDENT LOANS

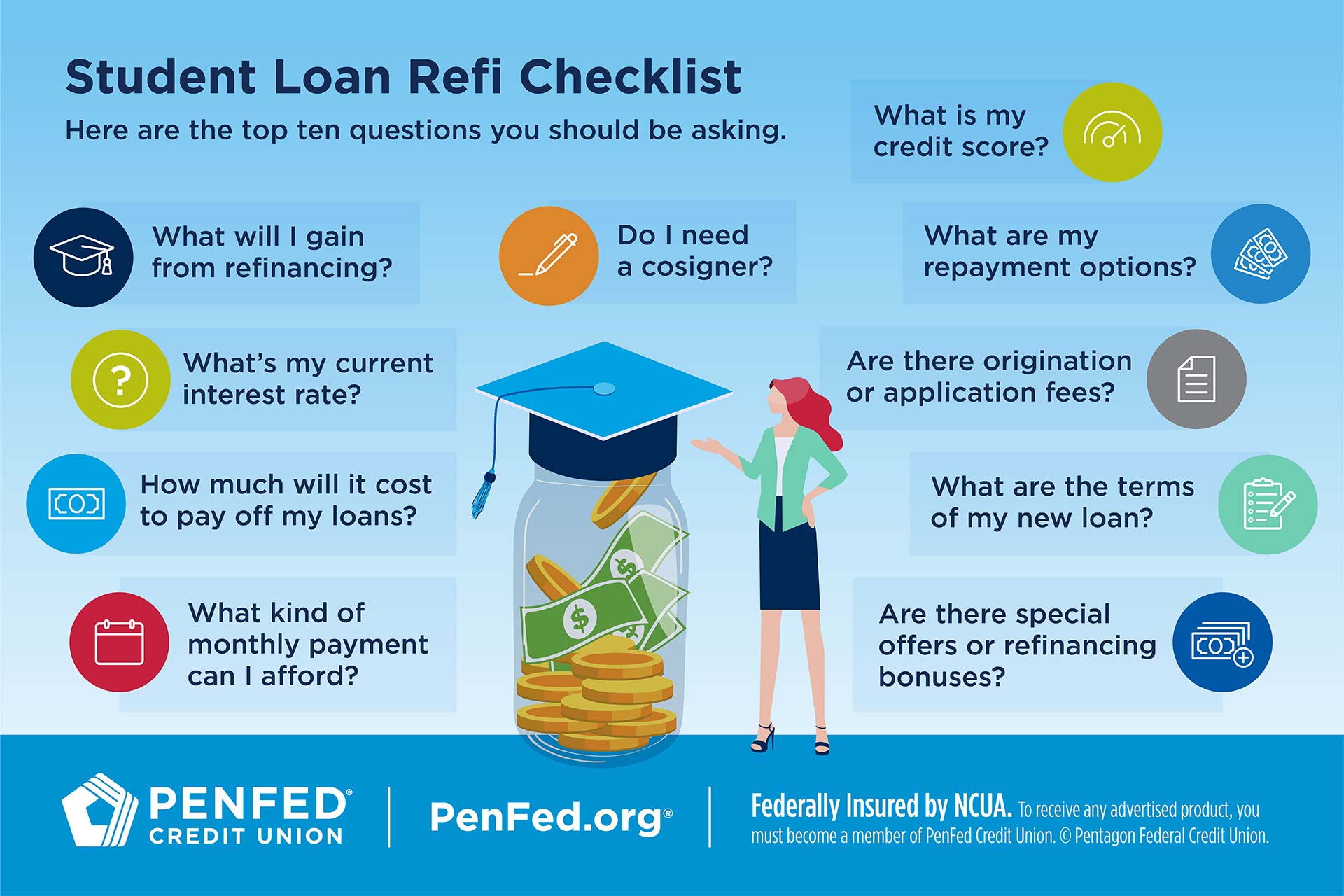

13 Questions to Ask When Consolidating Student Loans

EXPECTED READ TIME:8 minutes

You have a lot of options when it comes to student loan refinancing. In fact, if you’re just starting your search for a lender, it can be challenging to narrow the list.

Keep in mind that there’s no single best option — different refinancing opportunities meet different people’s needs. One thing is for sure, you’re more likely to find a good refinancing opportunity if you know what you want.

We’ll teach you how to ask the right questions — of yourself and your lender — to end up with the perfect refinance option.

What to Ask Yourself About Refinancing

If you’ve got any sort of debt, refinancing is probably one of your larger financial goals. If you’re carrying any share of the nation’s $1.58 trillion in student loan debt, that plan is likely going to include student loans. Here are eight questions to ask yourself for some much-needed clarity — before you talk to lenders:

1. What Will I Gain From Refinancing?

Maybe you’re tired of having five different payment due dates and would rather consolidate all your loans into one. Or maybe you want smaller monthly payments.

Whatever your reason, make a plan to stick to your refinancing goals. Different lenders offer different terms. Some may offer terms that meet your goals better than others and knowing your endgame can help you narrow the choices faster.

2. What Kinds of Loans Do I Have?

There are big differences between federal and private student loans. For most people, federal student loans offer better terms due to their low interest rates, flexible repayment plans, and forbearance in times of illness or financial crisis. Additionally, some borrowers may qualify for loan forgiveness if they work for certain government or nonprofit employers.

Unless you take out a Direct Consolidation Loan from the federal government, you’ll refinance your federal student loans with a private lender. That means losing your federal loan benefits. In some cases, refinancing might be worth it, but it’s important to consider what you’re giving up. If you still have a lot to pay off, consider a few things before refinancing:

- Would switching to a different federal repayment plan meet your needs better than refinancing?

- Would an income-driven repayment (IDR) plan be a good solution for you?

- Are you eligible for Public Service Loan Forgiveness (PSLF)?

- Can you find a more competitive interest rate than your federal loans offer?

- Is there a chance you might need forbearance if you lose your job or get sick?

Whatever your reason, make a plan to stick to your refinancing goals.

3. What Kind of Interest Do I Have on My Current Loans?

One of the major reasons people choose to refinance their student loans is to get a lower interest rate. Even if that’s not your primary concern, it’s important to compare your current interest rate to the rate you’d have if you refinance.

Another consideration is whether your current loans have fixed or variable interest rates. A fixed interest rate is set when you initiate a loan and doesn’t change throughout the life of a loan. In contrast, a variable rate will change in response to fluctuations in the economy and indexes like the prime rate. If your variable interest rate goes up, your payments will go up, too.

Fixed interest rates are usually better than variable rates for long-term debt like student loans, car payments, and mortgages because you know what you’ll be paying and can budget for that expense.

Fixed interest rates are usually better than variable rates for long-term debt like student loans.

4. How Much Will It Cost to Pay Off My Loans Including Interest?

Often when we think of student loan debt, we think about the amount we borrowed. But when you factor in interest, the amount you pay for a loan can be much more. For instance, say you borrowed $20,000 in student loans at an interest rate of 3.73%. At the end of 20 years, you’d have paid $28,409.

It’s helpful to know the actual cost of repaying your loans before you start comparing lenders for refinancing. That way you can compare the cost of your refinanced loan to your current terms to determine how much (if any) money you’ll save.

Let’s consider that $20,000 student loan debt again. You might think it’s a great deal if a lender offers to let you refinance at 3.50% interest for 24 years, but over the life of the loan you’ll actually end up paying $29,590 — a whole $1,181 more. This is because you’ll be paying interest charges on the loan for longer and that interest adds up.

5. What Kind of Monthly Payments can I Afford?

Many people turn to refinancing for smaller monthly payments. By increasing the term (or length) of your loan, you can spread your payments out and make them more manageable. This can help a lot if you lose your job or experience financial hardship.

On the flip side, the longer you pay on a loan the more you pay in interest. Spend too long repaying your loan and you’ll end up paying much, much more overall.

Figure out a happy medium between the size of your monthly payments and your increasing interest costs. Your payments shouldn’t be so much that you struggle to make them, but they also shouldn’t be so small that you aren’t making progress on paying off your loans.

Figure out a happy medium between the size of your monthly payments and your increasing interest costs.

6. What Is My Credit Score?

You’ll have to qualify in order to refinance your student loans. Part of qualifying involves having the minimum credit score set by your lender. Every lender sets their own requirements for qualifying, but most look for a 670 or better. Of course, the higher your credit score, the better the terms you’ll be offered.

If your credit score isn’t where it needs to be, you might choose to wait, improve your credit score, and then apply for refinancing.

7. Do I Need a Cosigner?

Qualifying for student loan refinancing can be a challenge. Many borrowers have a short credit history, short work history, and lower income working against them.

One way to overcome this is to find a cosigner. Usually a cosigner is a spouse, parent, or family member who agrees to pay a debt if the borrower cannot. Ideally, your cosigner should have a stronger credit score and/or higher income than yours to make your application more creditworthy. You can add a cosigner when you refinance your loan by adding the cosigner to your application when you first apply.

You must discuss this step with your cosigner before you apply for refinancing. Becoming a cosigner will impact that person’s credit score and will make them liable for your debt if you are unable to pay. Make sure your cosigner is comfortable with this before you begin the application process.

What to Ask Potential Lenders

Once you know what you’re looking for in refinancing, it’s time to talk with lenders to find the right offer. It’s important to investigate multiple lenders since each lender sets their own terms and some will be better for your situation than others.

It’s also important to get some quotes and ask questions before committing to a lender. You’ll undergo a hard credit inquiry when you apply for refinancing, which will temporarily lower your credit score. To limit the impact on your credit score, do your research and only apply to lenders you’re serious about.

8. What Repayment Options are Available?

A term is the length of time you have to pay back a loan. Longer terms usually mean smaller, more manageable monthly payments. However, you’ll pay more total interest the longer you pay on a loan.

If you’re looking to pay off your loan quickly, then you should prioritize an interest rate reduction to save money — but expect larger monthly payments with this strategy. If you’re refinancing to get smaller monthly payments, then a longer term will fit your goals better.

When possible, opt for a lender that offers flexible repayment terms. That way you can negotiate a loan term that meets your financial situation.

To limit the impact on your credit score, do your research and only apply to lenders you’re serious about.

9. Are There Origination or Application Fees?

While most lenders do not charge origination or application fees for refinancing student loans, some do. Usually, the origination fee is a percentage of the total amount of your loan, but that percentage is set by the individual lender so you’ll have to ask to find out how much it is.

You should take these fees into account when calculating the total cost of refinancing. For instance, if you’re charged a 3% origination fee for refinancing $20,000 in loans, that would add $600 to your costs.

10. Do You Have Any Special Offers or Refinancing Bonuses?

Some lenders offer borrowers incentives for refinancing. Incentives might include cash back, gift cards, or an introductory rate. Sometimes these bonuses can be a great way to jumpstart your savings or cut your grocery for a while. Just keep in mind that the terms of your loan are the most important factor when choosing a lender.

If you’re looking to pay off your loan quickly, then you should prioritize an interest rate reduction.

11. What Are the Terms and Conditions of My New Loan?

Once you’re serious about a lender, it’s time to get the specifics on how your new loan will work. Ask questions and keep track of important details. You should ask:

- When will my payments start?

- How will I make my payments?

- Are there fees for paying certain ways (such as by check)? Are any payment methods free?

- How much do you charge for late or missed payments?

- Do you offer any kind of forbearance or grace period during a financial crisis (such as job loss or serious illness)?

- Do you charge any penalties for paying off my loan early?

Before You Commit to a New Lender

Great terms can be exciting, but they don’t make up for bad customer service. Before you commit to a new lender, check out their reviews. A student loan is considered long-term debt and it may be years between the time you refinance and the time you pay it off. If the unexpected happens, you want a lender who will work with you.

12. What Kind of Reviews Does this Lender Have?

Do their customers complain about payments not being applied correctly? Unexpected or hidden fees? Misleading information? Missing paperwork? If so, move on.

What are some other warning signs to look for? Beware if a lender:

- Pushes you to commit before you feel confident

- Doesn’t give clear, easily-understood answers to your questions

- Can’t provide a complete list of fees associated with your loan

- Doesn’t require a credit check

- Offers terms that are unusually good compared to other lenders

Before you commit to a new lender, check out their reviews.

13. Does this Lender Offer Good Customer Service?

Maybe your autopay didn’t come out this month and you want to make sure you pay on time manually — or maybe you have an important question.

When these things happen, you want to be able to reach your lender and fix things quickly. While reading a lender's reviews, pay attention to how they make their customers feel. Do they fix mistakes quickly? Are they able to make accommodations for a borrower’s situation? If not, they’re not the right lender for you.

Every lender sets their own requirements for qualifying, but most look for a 670 or better.

The Takeaway

There’s nothing like making a big financial decision with confidence. When you see your student loan refinancing as a part of your overall fiscal goals, it makes choosing a lender, terms, and conditions simpler and moves you close toward financial freedom.