MORTGAGE KNOWLEDGE CENTER

PenFed Mortgage with Confidence

MORTGAGE

All About VA Loans and Your Credit

What you'll learn: How your credit score can affect your VA loan rate

EXPECTED READ TIME: 5 MINUTES

February 22, 2021

When you’re preparing to get a mortgage, your first choice is most likely a VA loan if you're a veteran. The rates are generally lower. Plus, in many cases, you can get into a home with zero money down. Like with any loan, there are specific credit guidelines that are good for borrowers to know. This article will go over some of the most common questions we get asked, including what credit scores you need with a VA loan, if you can get a VA loan or buy a home with bad credit, and what credit score is good for a VA loan. By the end of this article, you’ll have a better idea of what you need to do to receive a VA mortgage and become a homeowner.

What are some factors that may affect my credit?

Numerous things can adversely affect your credit and ultimately affect your rate when looking to get a VA loan.

- Late Mortgage Payments. If you previously have had late mortgage payments, that is a potential sign to a lender that you may be late again. If you’re looking to refinance, you can’t have a 30-day or greater late payment within the last six months.

- No Credit History. If you haven’t built up enough accounts to show you can handle credit, that can affect your overall score. The lender will be looking for patterns that demonstrate your ability to pay on time. If you don’t have traditional credit like loans or credit cards, the lender may consider other types of payments like rent, utilities, or a cell phone account to establish that you pay your bills on time.

- Bankruptcy. Either Chapter 7 or Chapter 13 bankruptcy within the last one to two years can affect your credit. Bankruptcies prior to two years are disregarded. However, for a VA loan, it's possible to use your benefits again, assuming you've been able to re-establish credit and prove excellent credit since.

- Collections. If you have multiple collection accounts, they may need to be paid off before you get a mortgage. However, each borrower’s credit file is reviewed as a whole. Also, borrowers with a history of collections will need to re-establish good credit before getting a loan.

- Federal Debt. If you have federal debt such as tax debt, this will adversely affect your credit. Any delinquent federal debts will need to be resolved before getting a mortgage. In some cases, making payment arrangements will suffice.

- Foreclosure. A past foreclosure on your property is another challenge that can affect your credit score. Generally, if the foreclosure was over two years ago, it can be disregarded. If it were between one to two years ago, you would need to provide more information.

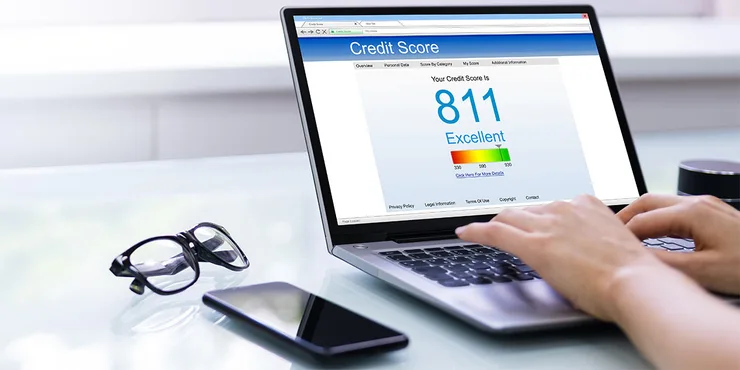

What do the credit score ratings mean?

Taking the time to get your credit to a strong level prior to purchasing a home is a great idea. But your credit doesn’t have to be perfect or even excellent. PenFed requires a minimum score of 620 for mortgage borrowers. So, don’t feel that you have to wait until your score is in the 700s. And especially when rates are low, it’s essential to try and get a loan as soon as possible.

Here are some typical credit scores and what the numbers can reflect:

|

300 - 499 |

Very Poor |

|

579 - 500 |

Poor |

|

580 - 669 |

Fair |

|

670 - 739 |

Good |

|

740 - 799 |

Very Good |

|

800 - 850 |

Excellent |

As you move up into each better credit category, your potential interest rate could lower. That’s because, the better credit you have, the less risk you are to a lender. They are also willing to provide you with a lower rate allowing you to pay less for your home over time.

You must consider the following. If rates are at record lows, you don’t want to hold off applying for a loan if your score is at least 620. So, what is the answer to what credit score is good for a VA loan? Once you’re close to 620, you’re on your way. While you could be working towards “excellent credit,” — you risk rates going up. So as soon as you’re close to being able to qualify, contact a mortgage professional at PenFed.

Can I get a VA loan with a bad credit score?

As outlined above, it's possible, but you may need to raise your score first. Depending upon your situation — it can be difficult if your score is very low. In many cases, with hard work towards improving your credit — it can happen. Remember, it is the purpose of the VA to help veterans achieve the goal of homeownership. If you’re not already there, getting your credit score to 620 and above is achievable. So, can you buy a home with a bad credit score? Not immediately with the VA, but don’t give up hope. You just need to work on improving your credit.

How can I improve my credit to get a VA loan?

There are some ways you can have an almost immediate impact on improving your credit score.

- Make all of your payments on time. This is extremely important because the lender will be looking to make sure you don’t have any late payments within the last 12 months, and if you do, they will require an explanation.

- Check with each credit agency to ensure their data is correct. It's not uncommon for an agency to have incorrect data that you can easily dispute and get corrected. That will have a positive impact on your credit score if you've removed any errors affecting your credit. It’s easy to get your free annual credit report to see if there is anything to fix.

- Pay down your debt. While this may sound obvious, there are two ways you can do this to improve your credit score. The first is to simply reduce the overall debt you have and pay down your balances. That will save you money in the long run, of course.

- Reduce your credit usage. The second way is to reduce the ratio of debt to available balances. For example, if you have a credit card with a $5,000 limit and have $4,500 in debt on that card, you have a high debt ratio to available credit. Reducing that ratio can improve your score.

- Don't apply for more debt. Leading up to a home purchase; you should be reducing any credit triggers or pulls on your credit. Any time you look into a credit card, a new car, or other large purchases, you may get a pull on your credit, which can be seen as possibly increasing your debt overall.

- Don’t close accounts. Closing credit card accounts (especially ones you’ve had for years) can plummet your score. So, keep the accounts open even if you’ve paid them off.

- Seek advice if you need help. There are lots of great free resources available to help you increase your credit. Even the Federal Trade Commission (FTC) has excellent resources about how to improve your credit.

Now that you’ve learned what credit score is suitable for a VA loan — take your next step, whether it’s working on your credit or talking to a mortgage professional today.

For more information about PenFed Mortgages:

PenFed Mortgage:

833-972-0244

SIMILAR ARTICLES

What Is a VA Loan?

What Is a VA Loan?

If you are wondering if you should apply for a VA loan, PenFed Credit Union is here to explain what a VA loan is, the benefits of a VA loan, and how to apply.

What Is a Conventional Loan?

What Is a Conventional Loan?

Conventional loans are just one type of mortgage loan. PenFed is here to help you understand what a conventional loan is and if it is right for you.

What Is a Conforming Loan?

What Is a Conforming Loan?

A conforming loan is based on guidelines set by government sponsored entities. It is important to understand what a conforming loan is and its differences from other mortgage loans.

What Are the Pros and Cons of VA Loans?

What Are the Pros and Cons of VA Loans?

VA loans can be beneficial because of low interest rates, no mortgage insurance requirements, and little to no down payment. PenFed helps you understand the pros and cons of VA loans.

Home Buying Steps

Mortgage Products

Disclosures

*Conventional Loans

Except for holidays, rates are updated Monday through Friday at 10:15am EST. The advertised rates and points are subject to change. The information provided is based on 1.25 discount point, which equals 1.25 percent of the loan amount, and assumes the purpose of the loan is to purchase a property with a 30-year, conforming, fixed-rate loan. Loan amount of $400,000; loan-to-value ratio of 75%; credit score of 760; and DTI of 18% or less. The property is an existing single-family home and will be used as a primary residence. The advertised rates are based on certain assumptions and loan scenarios, and the rate you may receive will depend on your individual circumstances, including your credit history, loan amount, down payment, and our internal credit criteria. Other rates, points, and terms may be available. All loans are subject to credit and property approval.

Rates quoted require a loan origination fee of 1%; not to exceed $1,995. Speak to a PenFed Mortgage Loan Officer for additional details.

**FHA Loans

Except for holidays, rates are updated Monday through Friday at 10:15am EST. The advertised rates and points are subject to change. The information provided is based on 1.375 discount point, which equals 1.375 percent of the loan amount, and assumes the purpose of the loan is to purchase a property with a 30-year, conforming, fixed-rate loan. Loan amount of $400,000; loan-to-value ratio of 96.5%; credit score of 760; and DTI of 18% or less. The property is an existing single-family home and will be used as a primary residence. The advertised rates are based on certain assumptions and loan scenarios, and the rate you may receive will depend on your individual circumstances, including your credit history, loan amount, down payment, and our internal credit criteria. Other rates, points, and terms may be available. All loans are subject to credit and property approval.

Rates quoted require a loan origination fee of 1%; not to exceed $1,995. Speak to a PenFed Mortgage Loan Officer for additional details.

***VA Loans

Except for holidays, rates are updated Monday through Friday at 10:15am EST. The advertised rates and points are subject to change. The information provided is based on 1.0 discount point, which equals 1.0 percent of the loan amount, and assumes the purpose of the loan is to purchase a property with a 30-year, conforming, fixed-rate loan. Loan amount of $450,000; loan-to-value ratio of 95%; credit score of 760; and DTI of 18% or less. The property is an existing single-family home and will be used as a primary residence. The advertised rates are based on certain assumptions and loan scenarios, and the rate you may receive will depend on your individual circumstances, including your credit history, loan amount, down payment, and our internal credit criteria. Other rates, points, and terms may be available. All loans are subject to credit and property approval.

Rates quoted require a loan origination fee of $995.

****Jumbo Loans

Except for holidays, rates are updated Monday through Friday at 10:15am EST. The advertised rates and points are subject to change. The information provided is based on 1.0 discount point, which equals 1.0 percent of the loan amount, and assumes the purpose of the loan is to purchase a property with a 30-year, non-conforming, fixed-rate loan. Loan amount of $1,009,000; loan-to-value ratio of 70%; credit score of 760; and DTI of 18% or less. The property is an existing single-family home and will be used as a primary residence. The advertised rates are based on certain assumptions and loan scenarios, and the rate you may receive will depend on your individual circumstances, including your credit history, loan amount, down payment, and our internal credit criteria. Other rates, points, and terms may be available. All loans are subject to credit and property approval.

Rates quoted require a loan origination fee of 1%; not to exceed $1,995. Speak to a PenFed Mortgage Loan Officer for additional details.

Fixed Rate Advance Lock-In You may lock in an Annual Percentage Rate for Advances during the Advance Period. During your Advance Period, you may choose to have three separate Fixed Rate Advances locked in at any one time, with a maximum of two new Fixed Rate Advances per calendar year. Each Fixed Rate Advance must equal or exceed Ten Thousand Dollars ($10,000.00) and you may not request a Fixed Rate Advance that would cause the amount you owe to exceed your Credit Limit. The only term option for your Fixed Rate Advance is 240 months (“Fixed Rate Advance Term”). However, the term of your Fixed Rate Advance cannot exceed your Repayment Period.

Routing #256078446

©2026 Pentagon Federal Credit Union